When examined with a wide lens, the stock market represents a pathway to long-term wealth creation. But when that lens is narrowed, the predictability of directional moves in the iconic Dow Jones Industrial Average (DJINDICES: ^DJI), benchmark S&P 500 (SNPINDEX: ^GSPC), and growth-powered Nasdaq Composite (NASDAQINDEX: ^IXIC) gets tossed out the window.

Although investors are reveling in the new bull market, the Dow Jones, S&P 500, and Nasdaq Composite have traded off bear and bull markets in successive years since 2020. There’s a real possibility this pattern persists in 2024, with stocks plunging, once again.

While there’s no such thing as a predictive indicator or economic data point that can, with 100% accuracy, forecast directional short-term moves in the Dow, S&P 500, and Nasdaq Composite, there are a few indicators and metrics that have strongly correlated with moves in the stock market throughout history. One such indicator, which has never been wrong, given a select set of circumstances, offers an ominous warning for investors in 2024.

This recession-forecasting tool has an impeccable track record dating back more than 60 years

Though “impeccable” is a word rarely thrown around on Wall Street, the Conference Board Leading Economic Index (LEI) has a truly impeccable track record of forecasting U.S. recessions.

The LEI is reported monthly (usually during the third week of a month) and contains 10 inputs. While three of these inputs are financial in nature, such as the performance of the S&P 500, the other seven are nonfinancial and include the likes of the ISM Manufacturing New Orders Index, average weekly manufacturing hours, and average weekly initial unemployment claims, to name a few.

The purpose of these variables is to predict changes in the U.S. business cycle. The Conference Board specifically states that the LEI is aiming to forecast “turning points in the business cycle by around seven months.” In other words, it’s attempting to predict recessions before they’re officially announced by the National Bureau of Economic Research.

In January, the LEI declined by 0.4%, which marked the 22nd consecutive month it’s contracted. That ties a period between 1973 and 1975 for the second-longest consecutive monthly downturn in the LEI, when back-tested to 1959. Only the 24-month contraction observed during the Great Recession (2007-2009) has lasted longer.

But it’s not the monthly declines that are most concerning. Historically, one-year comparisons have proved far more telling for the U.S. economy.

With regard to year-over-year changes in the LEI, the index has seen numerous declines that have ranged between 0.1% and 3.9% since 1959. While these drops shouldn’t be ignored, they’ve merely served as cautionary moments for investors and haven’t been indicative of a U.S. recession.

Here’s where things get interesting: Any time the LEI has declined by at least 4% on a year-over-year basis, a U.S. recession has eventually taken shape. There isn’t a single instance in the past 60 years when the LEI fell by at least 4% and the U.S. didn’t dip into a recession. As of January 2024, the LEI is down 7% from the prior-year period.

To be fair, stocks don’t necessarily mirror the performance of the U.S. economy. Wall Street tends to be forward-looking, which is why you often see the Dow, S&P 500, and Nasdaq Composite bottom out before the U.S. economy reaches its trough. Nevertheless, corporate earnings usually ebb and flow with the health of the U.S. economy. If the Conference Board LEI maintains its pristine streak of portending U.S. recessions, the broad expectation would be for stocks to plunge into a bear market.

Wall Street is priced for perfection (and that’s historically bad news, too)

The concern for investors is that the Conference Board LEI represents just one of a growing number of indicators and metrics cautioning of possible choppy waters for Wall Street in the not-too-distant future. In addition to declining M2 money supply, tighter bank-lending practices, and a heightened probability of a recession, based on the steepening of the Treasury yield curve, stocks are historically pricey.

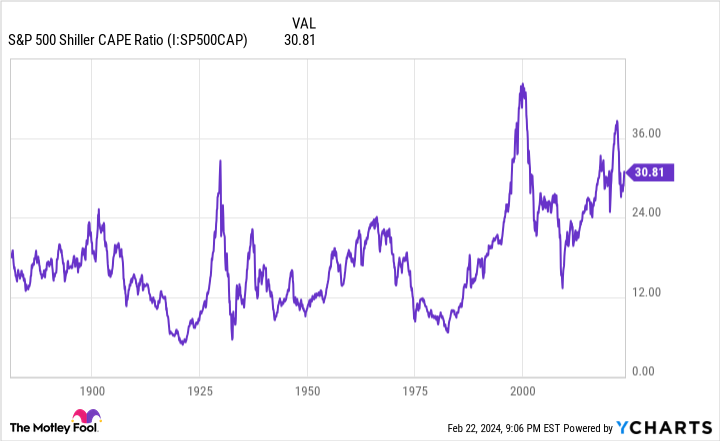

The valuation index that should be raising eyebrows at the moment is the S&P 500’s Shiller price-to-earnings (P/E) ratio, which is also known as the cyclically adjusted price-to-earnings ratio (CAPE ratio).

Whereas the traditional P/E ratio takes into account a company’s or index’s trailing-12-month earnings per share, the Shiller P/E for the S&P 500 is based on average inflation-adjusted earnings from the prior 10 years. Looking at 10 years’ worth of earnings history can smooth out the impact of one-time events, such as the COVID-19 pandemic, which temporarily skewed corporate earnings.

When back-tested to 1871, the Shiller P/E has averaged a reading of 17.09. However, it’s spent much of the past 30 years well above this mark. The democratization of information and access to trading, thanks to the advent of the internet, coupled with lower interest rates, has bid up valuation multiples for stocks as a whole.

But similar to the LEI, the Shiller P/E ratio has an arbitrary line-in-the-sand figure that’s historically represented trouble for investors. Specifically, it’s when the Shiller P/E ratio surpasses and sustains 30 during a bull market rally.

Looking back more than 150 years, there have only been six instances where the S&P 500’s Shiller P/E lifted above 30 and held this mark for a reasonable period. Following the five previous instances, the S&P 500 and/or Dow Jones Industrial Average went on to lose between 20% and 89% of their value. In other words, when valuations get extended to the upside, bear markets have historically followed. As of the closing bell on Thursday, Feb. 22, the Shiller P/E had surpassed 34.

To be transparent, the S&P 500’s Shiller P/E ratio isn’t a timing tool. This is to say that valuations can stay extended for a long time, just as they did for four years between 1997 and 2001. But the lesson history teaches is that extended valuations have led to eventual sizable pullbacks in the Dow, S&P 500, and Nasdaq Composite.

Now for the good news

Considering how strong the stock market has been over the past 14 months, the prospect of a plunge in stocks probably isn’t something investors want to think about. But I have good news on multiple fronts.

On one hand, U.S. recessions are a normal and inevitable part of the economic cycle. Since World War II ended in September 1945, the U.S. economy has worked its way through a dozen contractions. But here’s the thing: Nine of these 12 recessions lasted less than a year, and the remaining three failed to surpass 18 months in length. Economic downturns tend to be blips in the grand scheme of things.

By comparison, periods of economic expansion can stick around for a long time. Twice since September 1945, the U.S. economy has enjoyed a period of growth that hit the one-decade mark. Over extended periods, the American economy is going to expand — and it’s a similar story with the stock market.

Since 1950, the S&P 500 has endured 40 double-digit declines, which works out to a correction about once every 1.85 years. Despite never knowing ahead of time when these drops will occur, how long they’ll last, or where the trough will ultimately be, history has shown that each one of these double-digit declines was eventually fully recouped by a bull market rally.

A data set released by analysts at Bespoke Investment Group last year confirmed just how disproportionate bear markets and bull markets can be on Wall Street. Since the start of the Great Depression in September 1929, the average S&P 500 bear market has lasted 286 calendar days, or about 9.5 months. That compares to 1,011 calendar days for the average S&P 500 bull market over the same timeline.

Looking even further back yields more compelling data on the power of time and patience as an investor.

Every year, analysts at Crestmont Research update a data set that examines the rolling 20-year total returns, including dividends paid, of the S&P 500. Even though the S&P didn’t come into existence until 1923, its components could be located in other major indexes prior to its creation. This allowed Crestmont to back-test the S&P’s total returns to 1900, which led to 105 rolling 20-year periods of data (1919-2023).

The key finding is that none of the 105 rolling 20-year periods produced a negative total return. Hypothetically speaking, as long as an investor held their stake in the S&P 500 or an S&P 500 tracking index for 20 years, they would have made money every single time.

Therefore, patience and perspective are powerful tools when putting your money to work on Wall Street.

Where to invest $1,000 right now

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has nearly tripled the market.*

They just revealed what they believe are the 10 best stocks for investors to buy right now…

*Stock Advisor returns as of February 20, 2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Are Stocks About to Plunge? A Recession Indicator That’s Never Been Wrong Weighs In. was originally published by The Motley Fool