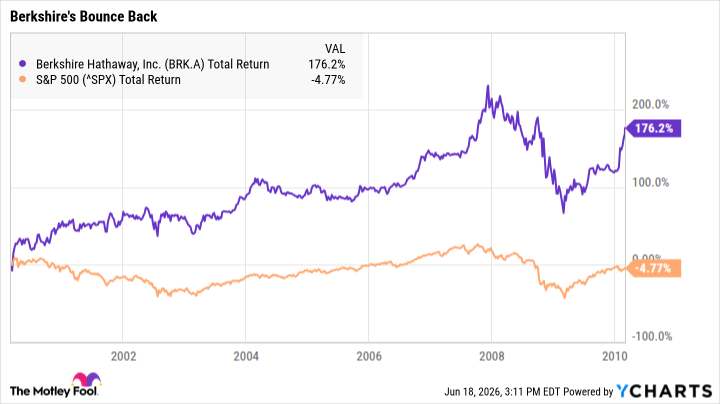

1999 was a bad year for Berkshire Hathaway (BRKA +0.68%) (BRKB +0.66%). Its book value per share increased by a measly half a percentage point. Its stock price tanked 20%. Meanwhile, the dot-com-fueled S&P 500 climbed 21%. It was the worst relative performance in any given year that Warren Buffett managed the company.

While Buffett took the blame for Berkshire’s significant underperformance, he also expressed confidence that his company would “modestly exceed” the benchmark index over the next decade. Buffett might have been too modest. Over the next decade, from the date Buffett published his 1999 letter to shareholders (March 3, 2000), Berkshire Hathaway stock returned 176%. The S&P 500 total return during that period was -4.8%.

BRK.A Total Return Level data by YCharts.

Today, Bill Ackman, a billionaire investor who has long looked up to Buffett, has likened a group of stocks to buying Berkshire Hathaway in 2000. While the S&P 500 is consistently pushing toward new highs, these stocks seem to be left behind by the market. Investors can buy them now at an incredible value and benefit for years to come.

Buy these “old-fashioned” companies

The biggest trend in the stock market over the last few years has been artificial intelligence (AI). And more recently, even more capital has flowed into very specific sectors related to the AI trade.

Semiconductor stocks have climbed higher as demand for graphics processing units (GPUs) and other AI accelerators continues to grow; the need for networking chips has come into focus; and memory chipmakers face a massive supply crunch. Energy stocks have also benefited as giant data centers consume gigawatts of power. Semiconductor stocks are up more than 90% this year alone, and energy stocks are up close to 60% as of this writing. For reference, the S&P 500 is up just 9% so far this year.

Meanwhile, the market has left the buyers of those products behind. Amazon (AMZN +1.55%), Meta Platforms (META 0.18%), and Microsoft (MSFT 0.21%) have fallen out of favor with investors, and Ackman believes that’s a mistake.

“People got excited about internet stocks and Berkshire Hathaway traded at the lowest valuation I think it ever traded at in its history,” Ackman said at a recent conference. “I think a similar thing is happening today in a sense to Amazon, and Meta, Microsoft. These are old-fashioned companies in kind of this OpenAI era.”

Today’s Change

Current Price

Indeed, Amazon and Microsoft operate the two largest public cloud platforms in the world. Their revenue is soaring as demand for AI compute grows, and they’re investing as much as they reasonably can to meet demand. They’re also using significant compute capacity for their own AI development, which fuels other parts of their businesses and drives revenue and operating profits.

Meta may have more to gain from advances in AI than any company. Its advertising business is already seeing strong performance from algorithm improvements across Facebook and Instagram. Ad revenue accelerated sharply in the first quarter. AI chatbots have the potential to turn WhatsApp into a sales and customer service hub for small businesses. And AI-assisted content creation could help serve more personalized images, videos, and advertisements to its 3.5 billion users.

Today’s Change

Current Price

Nonetheless, investors have concerns about their spending. Ackman takes the opposite stance. “When a business you own, managed by a management team you trust, announces a large increase in capital spending due to increased demand for its products or services, you should be applauding rather than booing.” Microsoft, Amazon, and Meta’s accelerating revenue growth is a strong indication that they’re making the smart decision with their spending plans.

Like buying Berkshire in 2000

One thing that allowed Berkshire Hathaway to dramatically outperform the S&P 500 in the 2000s was its starting valuation. The stock fell below 1.1 times book value in March of 2000. That’s the price Buffett would buy back shares of Berkshire Hathaway before the board changed its share-repurchase policy in 2018. In effect, it was a floor for the stock’s valuation. By 2010, the price-to-book ratio had expanded to nearly 1.5, and its book value had climbed quite substantially as well.

Today, Amazon, Microsoft, and Meta trade for price-to-earnings (P/E) ratios they’ve rarely seen before: 28, 22.5, and 18 times forward earnings expectations, respectively. That’s despite all three companies exhibiting strong revenue growth. While their massive capital expenditures will weigh on operating margin in the near term, they still have durable competitive advantages across their businesses, which should ensure long-term earnings power.

It wouldn’t be a surprise to see these stocks’ performances “modestly exceed” the market average over the next decade as earnings grow and the market rewards them with price-multiple expansion.