Veteran investors know the time to step into good stocks is after an erroneous sell-off. That’s why so many people are now eying Palo Alto Networks (NASDAQ: PANW) shares following Wednesday’s post-earnings dip. The 28% tumble is a huge discount on a solid company’s stock.

This is one of those cases, however, where interested investors might want to keep their powder dry for at least a few more days. This plunge is different than the typical setback for most stocks. It could linger, and perhaps even worsen before reversing course.

Investors are seeing the glass as half-empty

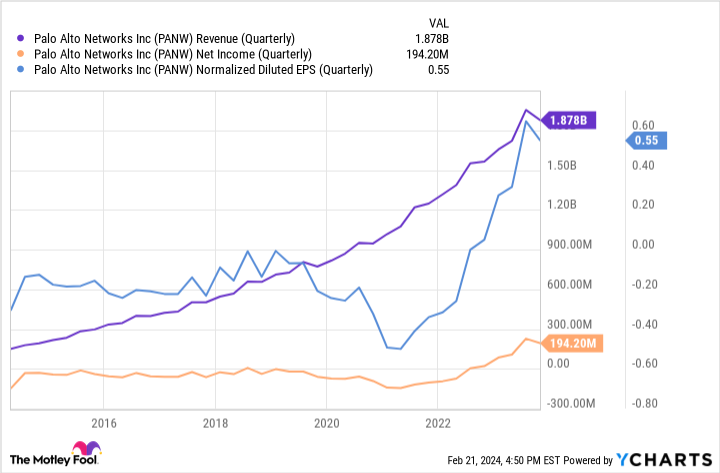

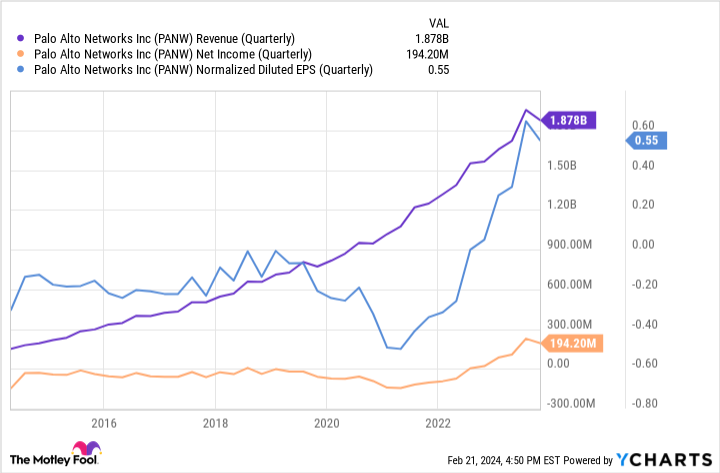

Cybersecurity outfit Palo Alto Networks reported its fiscal second-quarter 2024 numbers after Tuesday’s close. The top line grew to the tune of 19% to $2 billion in the period ended Dec. 31, 2023, and per-share profits of $1.46 were a marked improvement on the year-ago comparison of $1.05. Contracted revenue (for future booking) was up 22% year over year to $10.8 billion. Last quarter’s numbers were also better than analysts’ expectations.

The stumbling block? Guidance for the remainder of fiscal 2024. The company dialed it back for a second quarter in a row. Total full-year revenue is now expected to roll in between $7.95 billion and $8 billion. Half a year ago the revenue guidance was a range of $8.15 billion and $8.2 billion. Total billings should be lower than last August’s original forecasts as well. The market just panicked, fearing these revisions point to tougher headwinds on the horizon.

The sell-off is an overreaction though. As Palo Alto CEO Nikesh Arora explained during Tuesday’s earnings call, this lowered guidance reflects the company’s intentional “platformization” efforts. That is, adding several different products to a particular customer’s cloud-based software package for up to half a year at no additional charge. The hope is that these clients will like their new tools so much that they end up paying for access to them for at least several more years.

Investors, however, fear the tactic marks the beginning of a brutal price war that may never end.

Lost in all the noise is the fact that this sales tactic is actually quite cost-effective, since access to the cloud-based cybersecurity tools in question can be turned on and off by Palo Alto Networks with just a few keystrokes. In this same vein, also lost in Wednesday’s dust-up is that Palo Alto still raised its full-year profit outlook despite lower revenue guidance.

Then there’s the not-so-minor reality that this company is well equipped to fight any price war it may have just started.

It certainly sounds like a juicy buying opportunity. Just don’t be in too big of a hurry to take the plunge.

More than a knee-jerk reaction to lowered guidance

If you’ve already scooped up Palo Alto shares or if you can’t wait any longer, you’re not doomed.

Wednesday’s steep pullback isn’t your typical post-earnings stumble though, for handful of reasons. Chief among these reasons is the marketwide backdrop itself. It’s not great.

See, stocks have been rallying since October on hopes that the global economy was headed for a soft landing, ushered in by waning inflation and a subsequent series of gradual rate cuts. Now it’s not clear that’s what’s in the cards. Inflation isn’t exactly cooling off as quickly as hoped, nor is the Federal Reserve as keen on lowering interest rates as quickly as expected.

Shellshocked investors are suddenly rethinking all of their purchases. Following their 50% three-month run-up, Palo Alto Networks shares may have been especially vulnerable to even the slightest of missteps from the broad market.

The lowered guidance may also be serving as a wakeup call to shareholders regarding Palo Alto’s valuation — even though its underlying earnings aren’t expected impacted by the aforementioned top-line lull.

It’s curious. Sometimes the market’s willing to overlook an outrageous valuation as long as the growth story remains perfectly intact. That’s been Palo Alto for years now. Investors didn’t mind its regular losses all the way through 2021, knowing it was making progress toward profits. That finally happened in 2022, and those profits have widened in the meantime.

The kind of money Palo Alto Networks is now making, though, is in the same ballpark as the kind of money it’s going to be able to earn a few years from now. With shares priced at more than 40 times this year’s projected profits and more than 30 times 2026’s expected per-share earnings of $7.93, all of a sudden the premium valuation doesn’t feel so comfortable. It happens.

Finally, Palo Alto’s announcement didn’t just catch investors off guard. It surprised analysts, too. Not too many of them outright downgraded the stock, but several analysts weighed in with lowered price targets. Don’t be surprised to see a few more follow suit in the near future, as they digest the company’s sales strategy and what it may mean for the entire cybersecurity business. This could keep the narrative leaning in a bearish direction for at least a few more days.

All of these stumbling blocks, however, are temporary.

But Palo Alto stock is still a buy — sooner or later

Investors are still generally better served by not trying to perfectly time the market. Nobody does it very well for very long. It often ends up hurting more than helping, in fact.

That’s not what this is though. Taking a pause before plunging into any new Palo Alto position isn’t an attempt to time the market as much as it is a means of managing risk by allowing the post-earnings effect to run its full course.

Doing so might work in your favor, or it may work against you. Palo Alto Networks stock is in a scenario it’s never really been in before. That’s why you must resist the temptation to be one of the first ones to try and catch this falling knife, so to speak.

But how long should you wait to make any purchase? Give it at least a week, but there’s no need to wait longer than a month if you’re certain you want to own it for the long haul.

By the way, Precedence Research says the global cybersecurity market is poised to grow at an annualized pace of 12.6% through 2032. That’s not an opportunity you want to miss out on.

Should you invest $1,000 in Palo Alto Networks right now?

Before you buy stock in Palo Alto Networks, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palo Alto Networks wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 20, 2024

James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palo Alto Networks. The Motley Fool has a disclosure policy.

Buy Palo Alto Networks Stock on This Dip — Just Not Yet was originally published by The Motley Fool