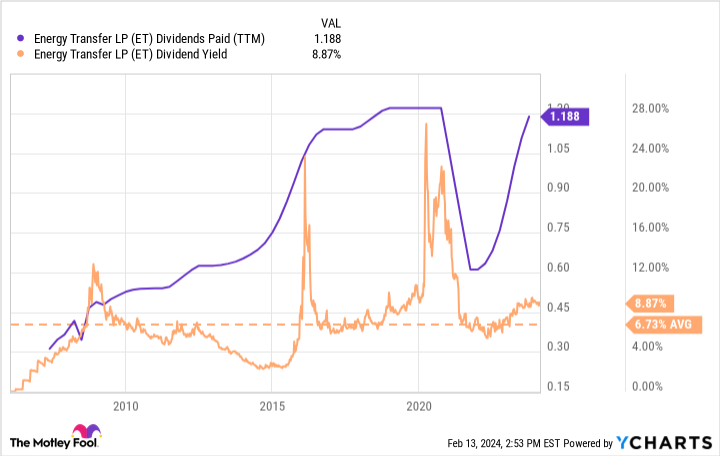

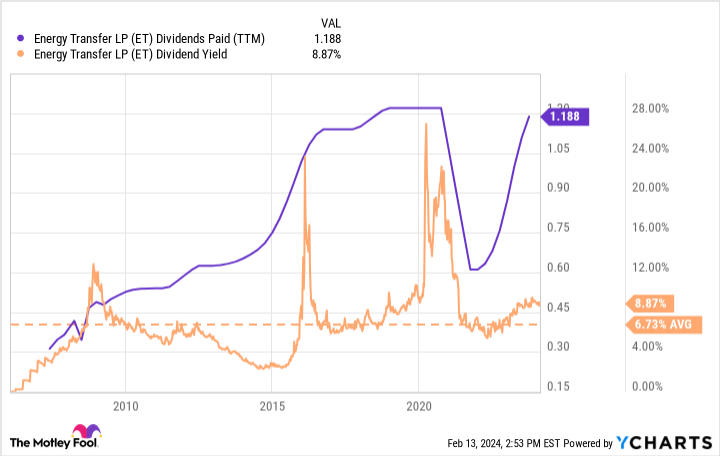

Few stocks are able to sustain 9% dividends, yet that’s exactly what Energy Transfer (NYSE: ET) did on February 6 when it increased its payout even though its dividend yield was already above 9%. And this isn’t the first time Energy Transfer has boosted its already-high dividend. The company has raised the payout every quarter for more than two years.

Is this your chance to secure a truly reliable 9% dividend yield?

This stock is built for income

Some businesses are built for growth, while others are designed to produce free cash flow. Energy Transfer is the latter type of business. It owns assets that, while expensive to initially construct, eventually generate high levels of extra cash, the reason for the stock’s high dividend over the years.

What exactly does Energy Transfer do? As its name suggests, it helps energy companies transfer their output from extraction sites to refineries, storage, and eventually the market. It deals mainly with crude oil and natural gas, owning pipeline and terminal assets throughout the U.S., with a particular focus on Texas and its neighboring states, which all have high levels of new fossil fuel production.

Assets like pipelines are capital intensive to construct. That means Energy Transfer must access the debt markets to get new projects up and running. Once built, however, the company often has a monopoly over its customer base. After all, pipelines are the most cost-effective way to transport most fossil fuel production. If there’s only one pipeline that services a particular area, then potential customers have little choice but to use it.

This market power typically allows Energy Transfer to set the rules. The company therefore generates around 90% of its cash flow on a fee basis, meaning its earnings are not tied to commodity prices, which can fluctuate a lot over the short term. Customers just pay for what they use in accordance with a preset fee schedule.

Stable cash flows have allowed the company to pay a steady dividend for more than a decade, the only exception being a temporary drop during the early days of the pandemic when it wasn’t clear how liquid capital markets would be. The dividend was suspended out of caution, not because the business was falling apart. . This year the company expects to generate at least $7 billion in distributable cash flow, around $1 billion more than it needs to support the dividend and near-term growth initiatives.

Why is the dividend yield so high?

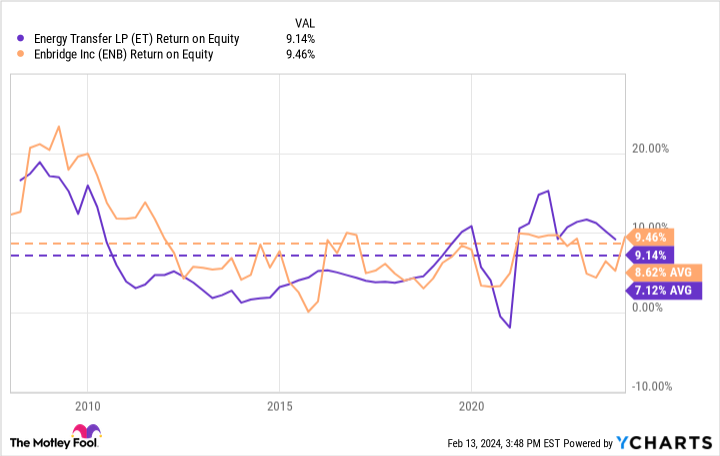

If Energy Transfer can sustain its 9% dividend, why isn’t the market bidding up the stock price to push the yield down to a more normal range? The issue is that companies that rely on fossil fuel production have been trading at a discount for years. Just look at Enbridge, a close competitor. Enbridge owns one of the largest pipeline networks in the world. It has a terrific track record of success, with high pricing power over its customer base. Yet its dividend yield is around 8%, even though the payout has grown by 10% annually for nearly 30 years.

The market’s wavering confidence isn’t due to unreliable dividends, nor is it caused by deteriorating business results. Both Energy Transfer and Enbridge have generated respectable returns on equity over the past decade or two, with recent results slightly above multi-year averages.

The market knows that these businesses are performing well, and that the current dividends are a bargain.

The issue is that these businesses may end up with stranded assets. That is, if regulations or market dynamics force a sudden shift away from oil and gas, pipeline operators will suddenly be left without any customers, with little else to do with their multi-billion dollar asset base.

This sudden shift in energy demand may eventually come to pass, but not for quite some time. Over the next few years, the EIA expects oil and gas consumption to steadily grow, though other groups like the IEA believe oil demand may begin to plateau in the 2030s.

Should you jump into Energy Transfer stock for the 9% dividend? With the exception of a global recession, the payout should remain stable, and likely for years to come. Just know that this is not a stock worth owning forever. At some point over the next century, the widespread replacement of fossil fuels with renewable sources of energy will present a growing headwind, one that will eventually pressure the dividend.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 12, 2024

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Enbridge. The Motley Fool has a disclosure policy.

Can Energy Transfer Stock Maintain Its 9% Dividend? was originally published by The Motley Fool