With mega-cap tech earnings out of the way, the stock market is quietly rejoining the Iran war trade.

- The S&P 500 stalled the moment the earnings tailwind faded, even as Palantir topped estimates

- Crude oil, Treasury yields, and the dollar are still stuck on the “war trade” stocks were ignoring

- ISM services PMI data and an RBA rate hike could amplify the hawkish global chorus this week

After three weeks of cheerfully erasing every implication of the US-Iran war, stocks started this week with an uncomfortable look at the rest of the asset complex. With mega-cap tech earnings done until Nvidia (NVDA) on May 20, the tailwind that powered the late-April melt-up has gone quiet and the “war trade” front and center in other markets seems to be back in focus.

Stocks rejoin the Iran war trade as the earnings tailwind fades

The bellwether S&P 500 stalled today, with much of the upside gap at the weekly trading open fading as the session wore on. The technical issues flagged last week remain glaring. Volumes have shrunk throughout the rebound from the wartime selloff. The relative strength index (RSI) momentum gauge shows negative divergence: prices set higher highs while the indicator does not. Conviction seems to be running out of steam.

The breakaway rally that erased the war’s damage and punched to new records lined up almost exactly with the start of mega-cap tech earnings. With Microsoft (MSFT), Alphabet (GOOG), Amazon (AMZN), Apple (AAPL), and META having now reported and the calendar quiet until Nvidia (NVDA), bullish enthusiasm has waned.

Palantir (PLTR) topped earnings forecasts overnight — overshooting analysts’ bets by 18% on EPS and 6% on revenue — and the markets shrugged. Shares seesawed higher, then lower in after-hours trade, only to settle little-changed. If the artificial intelligence (AI) growth story was as convincing as last week, these outcomes might have lit a fire.

Other markets never stopped trading the war

Crude oil is back near the top of its wartime range. Treasury bond prices are sliding as yields push higher, with sticky oil forcing interest rate expectations up across global central banks.

Gold is leaking lower as rising yields and a stronger US dollar make non-interest-bearing and anti-fiat assets less attractive. A suddenly circumspect tone on Wall Street is helping the greenback reassert itself.

Bitcoin remains an exception, quietly extending the upside breakout that began in early April.

The data center engine has obvious vulnerabilities

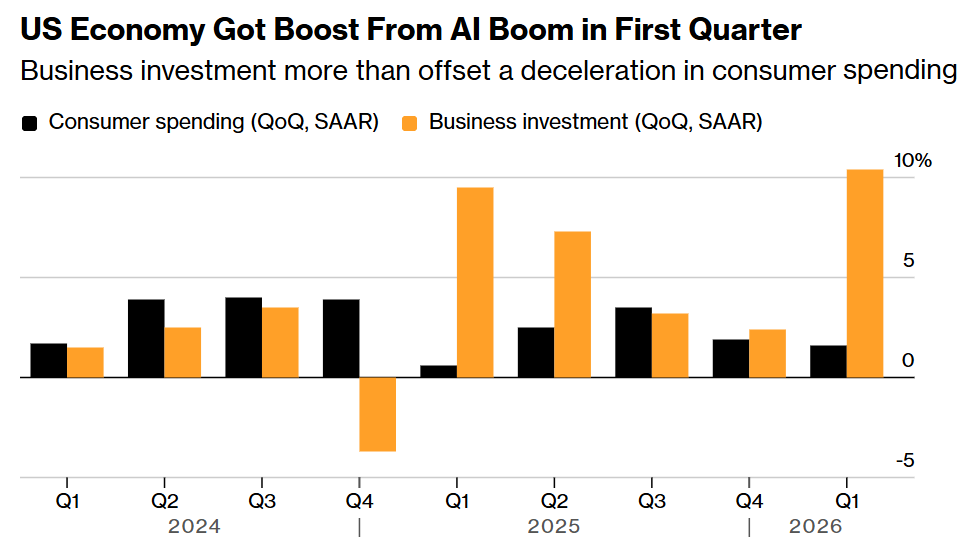

Last week’s first-quarter US gross domestic product (GDP) report made clear how heavily the economy is leaning on the AI buildout. Fixed nonresidential investment contributed 1.39 percentage points (ppt) to the 2% headline growth figure, edging out consumers at 1.08ppt.

Business investment grew at an annualized 10.4% in the first quarter, while consumption has decelerated for two quarters straight, growing at a rate of just 1.6%. That is how a small 14% slice of GDP – the investment bit – manages to outstrip the growth uplift from a meaty 68% slice – household consumption.

That math only holds while business investment keeps moving fast. The five Mag 7 names that reported last week touted some $750 billion in additional capex. The catch: AI supply chains are deeply internationalized, and the Strait of Hormuz — a chokepoint for vital inputs, energy and otherwise — remains effectively closed.

Even if the so-called AI “hyperscalers” splash out for materials to build data centers at any price, that itself feeds inflation, lifts rates, and tightens financing for both them and the consumer. That ought to make it devilishly hard to sustain first-quarter growth dynamics.

Inflation is broadening as central banks line up hawkish

Core inflation is perking even before the war’s oil shock is accounted for. Goods inflation is rising again as the rebasing away of tariff costs that the Federal Reserve was banking on proves to be elusive. Service-sector inflation is posting the largest monthly gains since mid-2025. Housing prices are climbing too.

The price growth shock from energy comes atop all that. It usually takes about one month for crude oil price swings to filter into headline US consumer price index (CPI) inflation data. Only the modest January and February run-up has shown up there so far. The bigger war-driven spike should begin to appear in April’s data, due for release next week.

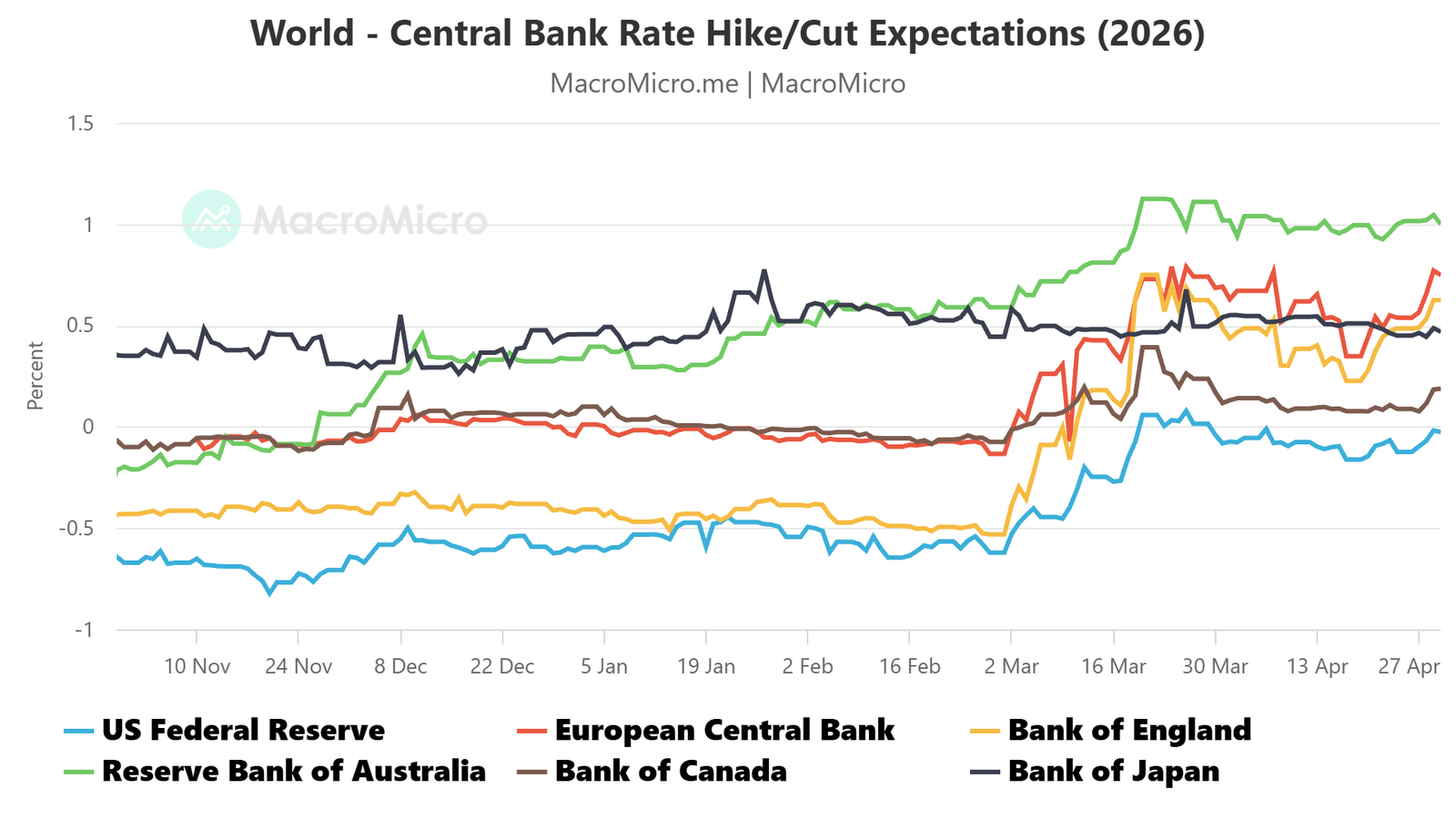

Markets now price 75 basis points (bps) of European Central Bank (ECB) rate hikes by year-end, more than 50bps from the Bank of England (BOE), and at least one hike from the Bank of Canada (BOC). The Fed is back to no cuts this year, with the priced-in odds of a hike outweighing those of a cut at every meeting through October 2027.

The Reserve Bank of Australia (RBA) is expected to deliver its first war-related rate hike at a policy meeting later today, marking its third consecutive 25bps increase this year. It is slated for a fourth one to follow before 2026 is out.

ISM services PMI data is the next test

Service sector purchasing managers index (PMI) data from the Institute for Supply Management (ISM) is the next test for markets.

Last week, the ISM manufacturing PMI print came in at 52.7 for April – effectively in line with forecasts calling for 53.0 and matching the March result. The headline probably matters less than the internals however: surging prices, shrinking employment, and softening new orders.

If the service-sector gauge paints a similar picture, inflation fears may get a boost as the case for rate cuts fades further. Stocks have spent three weeks blissfully ignoring all of this. Today may be the first hint that are ready to pay attention.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

© copyright 2013 – 2026 tastylive, Inc.