Fed Chair Powell put the brakes on the stocks last week. Since then, a listless market seems confused.

- Wall Street still seems shellshocked after last week’s FOMC policy announcement

- Fed Chair Powell spooked markets with a forceful push against rate cut speculation

- ISM service sector data and the UofM consumer confidence gauge are due ahead

Stock markets marked a clear diving line at last week’s monetary policy announcement from the Federal Reserve. Optimism prevailed before Fed Chair Jerome Powell took to the podium. It evaporated just minutes after that, and even now continues to elude traders.

The US central bank delivered a 25-basis-point (bps) rate cut as widely expected and its statement raised no eyebrows, despite sounding annoyed at the lack of economic data amid the government shutdown. But then, Chair Powell used the post-meeting press conference to forcefully push back on expectations of another rate cut in December.

Stocks hit a wall after Powell beat back December rate cut bets

The bellwether S&P 500 fell 0.97% on the following day, while the tech-tilted Nasdaq 100 shed 1.45%. Those were the sharpest losses for the two leading US equity benchmarks since the bloodbath on October 10. Prices have drifted sideways within narrowing ranges since then, as if the wind has gone from the markets’ sails.

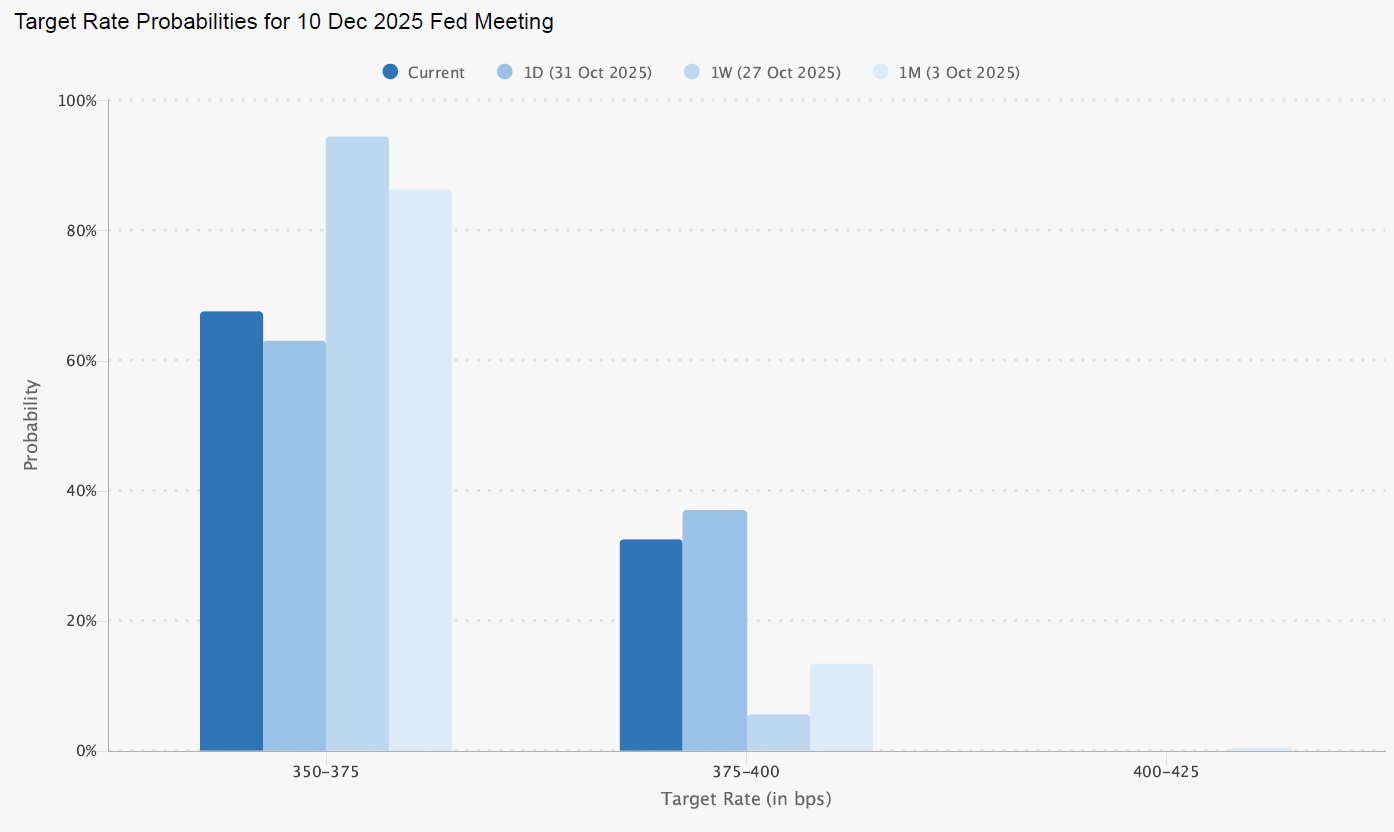

As it stands, the priced-in probability of a 25bps rate cut at next month’s gathering of the Federal Open Market Committee (FOMC) has come down to 65.3%, compared with a commanding 94.4% a week earlier. That still puts the odds in favor of more stimulus, but traders’ conviction in that outcome has been badly bruised.

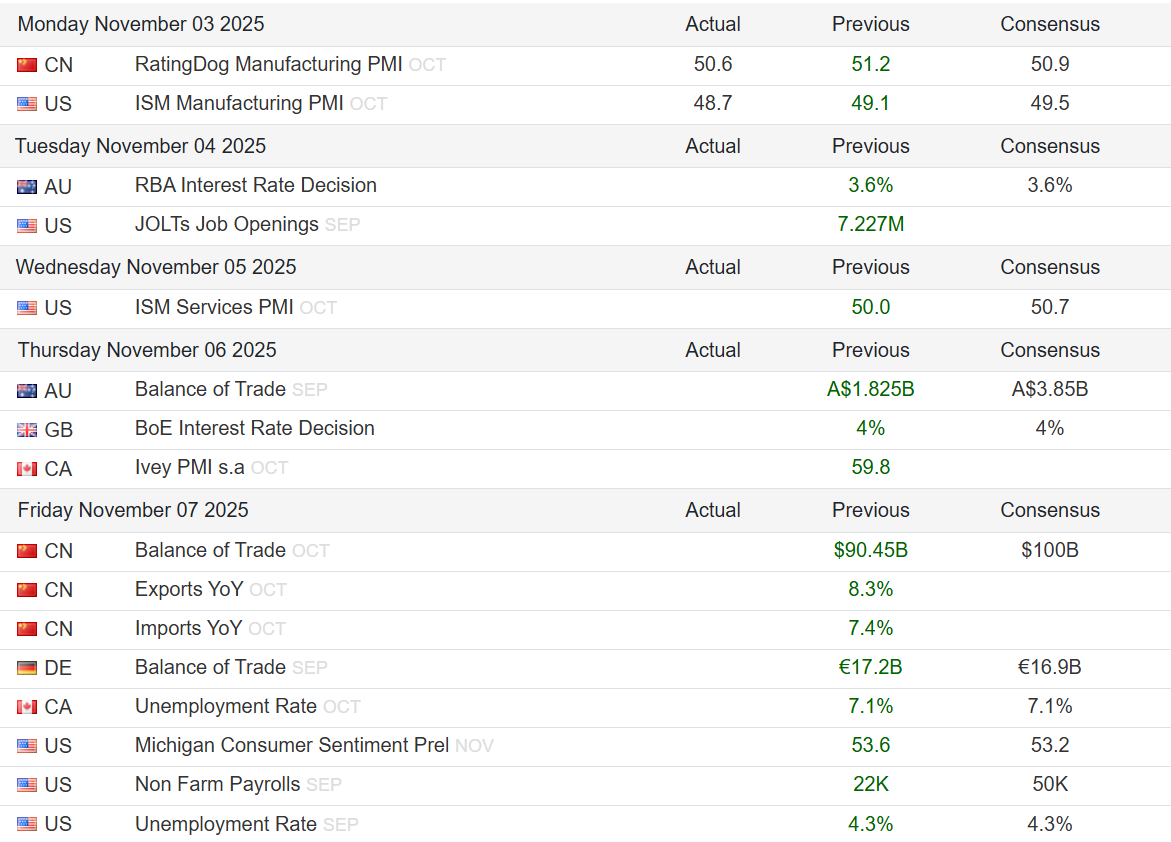

The US jobs report that ought to have come out this week now looks unlikely to appear as the government shutdown continues to disrupt data flow. An update on the service sector from the Institute of Supply Management (ISM) might serve as a stand-in. It is expected to show growth picked up a bit in October after standstill in September.

Private economic data in focus as US government shutdown drags on

An analog ISM report tracking manufacturing revealed a faster contraction in the pace of economic activity than analysts expected. New orders fell again in October after a loss in September, while employment shrank for the ninth month straight. Price growth slowed to the weakest since January, hinting at soggy demand.

Short of a budget breakthrough in Washington DC, that leaves the University of Michigan (UofM) gauge of US consumer confidence. Sentiment has been weakening since July, despite anchoring inflation expectations. It is projected to deteriorate further in November’s survey, falling to the gloomiest since May.

Outside the US, the Reserve Bank of Australia (RBA) and the Bank of England (BOE) are expected to keep interest rates unchanged when they deliver policy announcements this week. China will publish October’s trade statics. Early forecasts point to a slowdown in both exports and imports.

Ilya Spivak, tastylive head of global macro, has 15 years of experience in trading strategy, and he specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive or the YouTube channels tastylive (for options traders), and tastyliveTrending for stocks, futures, forex & macro.

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.