Robinhood is backing a push to scrap SEC Rule 611, a little-known rule meant to stop the market from skipping the best stock price investors can actually see.

The fight sounds technical. But it comes down to something basic. When the market shows a better stock price, should that price have to be respected?

The rule is SEC Rule 611, also known as the order-protection rule. The Securities and Exchange Commission has proposed rescinding it, and Robinhood (HOOD) is backing the move.

The debate has pulled in retail brokers, exchanges, market makers, Wall Street trade groups, and firms eyeing tokenized stocks.

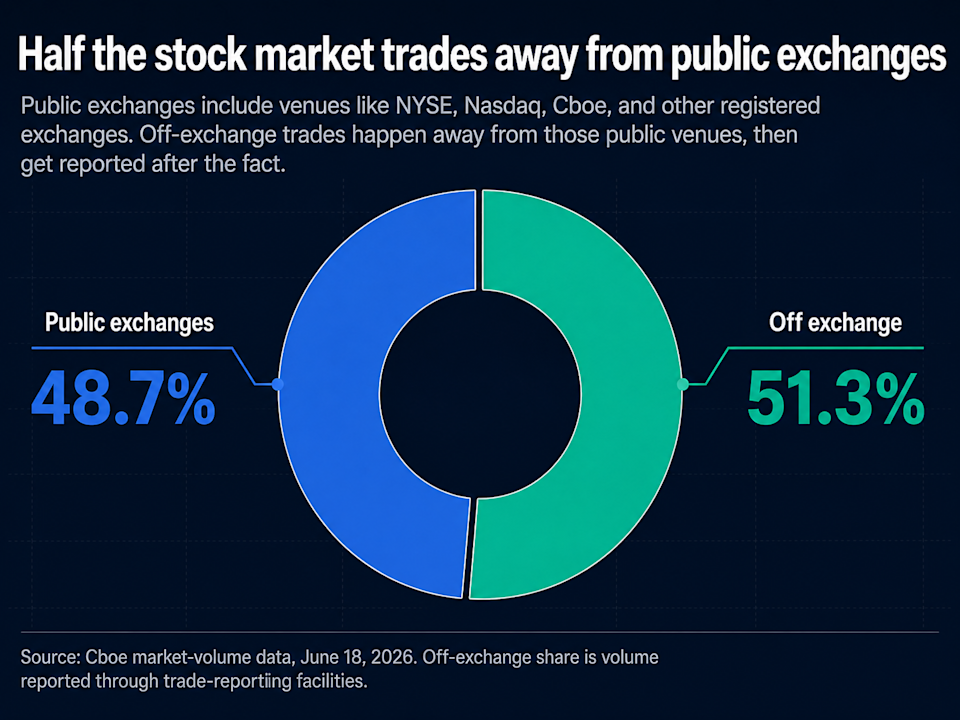

The SEC says the rule applies to hundreds of trading centers, from public stock exchanges to firms that execute trades away from those exchanges.

In plain English, Rule 611 is a best-price guardrail. If one trading venue is showing the best public price to buy or sell a stock, another venue generally cannot ignore that quote and execute at a worse price somewhere else.

That best public price is known as the national best bid and offer, or NBBO. Think of it as the market’s public scoreboard for the best price to buy and the best price to sell.

Robinhood’s case is modernization. The company argues the rule is outdated, adds complexity, and has helped spread trading across too many places. It says brokers would still have a duty to seek best execution for customers even without Rule 611.

That is the argument for change. The modern stock market is already a web of public exchanges, private trading systems, market-making firms, and off-exchange trading.

SEC Rule 611 applies across hundreds of trading centers in a market split across exchanges, private venues, and off-exchange firms.

Joe Saluzzi, co-founder of Themis Trading, sees the same sprawl and reaches the opposite conclusion.

“If you’re the best bid or the best offer, your price needed to be traded with before they can go to a different price,” Saluzzi told Yahoo Finance at the June ETP Forum hosted by ETFGlobal. “So it protects the best bids and offers.”

His concern is that replacing a bright-line rule with a broader best-execution standard could weaken the public quote investors rely on.

Saluzzi offered a simple example: Say the highest public offer to buy a stock is $10, while the lowest public offer to sell is $10.05. The $0.05 gap is the spread. If a retail investor offers to buy at $10.01, that investor is now showing the best bid.

Without Rule 611, Saluzzi said, “Your best bid could now get traded through.”

There is also a newer wrinkle. Saluzzi argues that the rule matters even more as regulators explore ways for tokenized stocks and other stock-like products to trade outside traditional market plumbing. A tokenized stock may track Apple (AAPL) or Nvidia (NVDA), but it is not the same as trading the company’s registered shares.