Recently, several investment banks have shifted their stance on Schrödinger (SDGR). Goldman Sachs has started coverage, while other firms such as Morgan Stanley and Citigroup have lowered their outlooks. These moves have put the company under renewed investor scrutiny.

See our latest analysis for Schrödinger.

Schrödinger’s muted share price returns this year suggest momentum is running low, with little reaction despite recent analyst downgrades and new coverage drawing attention. The latest share price sits at $21.45, but the one-year total shareholder return shows a modest gain of just 0.23%. Three- and five-year total shareholder returns remain negative, which keeps long-term investors cautious about a turnaround for now.

If market shakeups and shifting analyst sentiment have you considering fresh opportunities, it might be the perfect time to broaden your horizon and discover See the full list for free.

With sentiment split and analyst targets now implying a notable discount to the current price, investors must ask themselves if Schrödinger is flying under the radar or if the market is already factoring in future growth expectations.

Most Popular Narrative: 21% Undervalued

The current narrative suggests Schrödinger’s fair value sits well above its last closing price, hinting at significant upside potential if key drivers materialize. There is a notable gap between recent trading levels and the price target, and the debate centers around whether its future catalysts are powerful enough to reset market expectations.

Strong pipeline advancement and early clinical success, such as positive Phase I data for SGR-1505, positions the company to secure additional milestone payments, royalties, and out-licensing deals. This creates potential for substantial long-term revenue growth and more predictable future cash flows.

Curious what future product breakthroughs and bold expansion targets are included in this narrative’s calculus? There is a quantitative growth story and path to profit within the projections that could surprise investors. But the most controversial ingredient behind this valuation? Find out what’s driving such a confident outlook in the full narrative.

Result: Fair Value of $27.30 (UNDERVALUED)

Have a read of the narrative in full and understand what’s behind the forecasts.

However, persistent margin pressure and a heavy reliance on milestone revenues could quickly undermine the bullish outlook if clinical or customer growth stalls.

Find out about the key risks to this Schrödinger narrative.

Another View: Sales Ratio Perspective

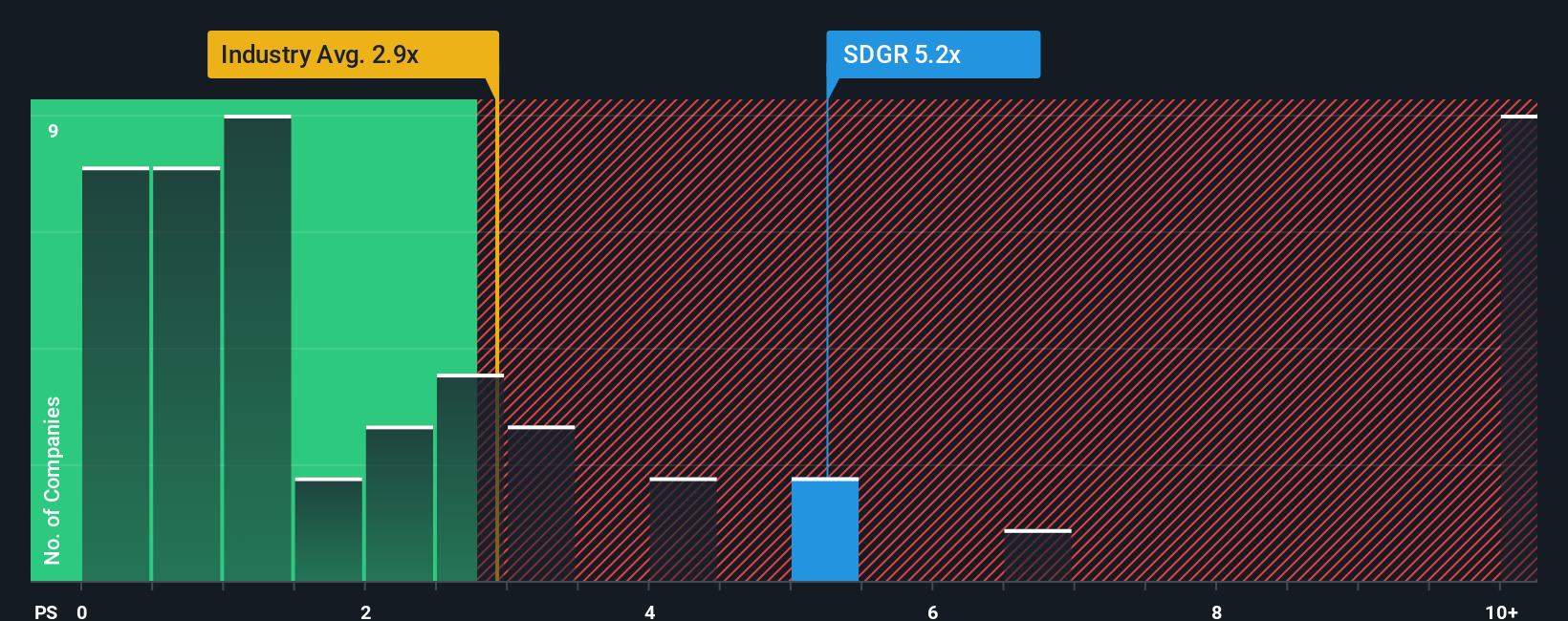

While fair value modeling paints Schrödinger as significantly undervalued, the company’s price-to-sales ratio tells a different story. At 6.6 times sales, Schrödinger is priced much higher than the US Healthcare Services industry average of 3 times and the peer average of 2.7 times. This gap suggests the market may be pricing in more growth than peers may achieve, or it could reflect greater risk if those expectations fall short. Is the premium truly justified, or could there be downside if results disappoint?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Schrödinger Narrative

If you see the story unfolding differently or want to challenge the data with your own perspective, you can craft your own research narrative in minutes. Do it your way

A great starting point for your Schrödinger research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Make your money work smarter for you by targeting stocks poised for explosive trends, untapped growth, or reliable income. Don’t let the next big opportunity slip past you just because you missed the right screener.

- Unlock bold growth by tapping into these 24 AI penny stocks to see which companies are reshaping entire industries with artificial intelligence leadership.

- Harvest steady returns and outpace inflation by checking out these 19 dividend stocks with yields > 3%, which offers consistently high yields backed by strong fundamentals.

- Get ahead of the crowd by exploring these 3564 penny stocks with strong financials; these may transform portfolios with their potential for dramatic price moves and breakthrough innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com