Stocks took some real lumps last week. Can the AI melt-up survive a week of Nvidia earnings, Fed meeting minutes, and global growth data?

- Friday’s drop in the S&P 500 came on the highest trading volume since April’s rally breakout

- Bonds are eyeing pre-tariff 2025 lows, which may bring yields back to growth-scare territory

- Three event risks this week could decide whether the “AI buildout trade” still has momentum

The blistering Wall Street rally that has powered the S&P 500 to record highs since early April finally showed cracks late last week. The bellwether index suffered its first meaningful down day in weeks Friday on the heaviest trading volume since the equities rally broke away from the “Iran war trade” guiding markets like crude oil, good, and the US dollar.

Stocks paused at the start of this week’s trade without committing in either direction. The reprieve looks tenuous as potent calendar of event risk unfurls over the next four sessions.

The technical issues casting doubt on stock market strength flagged earlier this month have escalated. Through early May the melt-up came on shrinking volume. Conviction seemingly drained as prices climbed. Last Friday flipped that pattern. The selloff arrived on the highest volume since the rally’s early-April breakout. That may signal something more than a passing pullback is brewing ahead.

Stocks stall but the “war trade” is breaking fresh ground

Monday’s Wall Street session offered no lasting recovery and no follow-through lower.

Still, crude oil resolved higher again after attempting a modest pullback in the opening hours of the trading week. Natural gas also climbed, with the broader energy complex now feeling renewed upward pressure. The Strait of Hormuz remains effectively closed, and damage to natural gas production facilities means it may take even longer to unwind supply disruptions there than for crude oil, once Washington and Tehran come to terms.

Treasury bond prices have continued to melt, with yields rising further. Prices have taken out the lows set during the original April ceasefire bounce, breaking to levels last seen in early 2025 before the growth scare triggered by the Trump administration’s rocky rollout of new tariffs. The US dollar is clinging to the top of last week’s range, while gold prices are struggling to mount a convincing rebound from the low end of its recent trading band. Neither market seems willing to give back Friday’s moves.

Last week’s economic data sounded the alarm for traders

Worries about what the Iran war will mean for inflation and interest rates escalated enough to force stocks to pay attention after last week’s Cerebras IPO. Traders may have been holding their breath for the landmark offering before turning their attention to the inflation and growth data piling up everywhere else in the financial system.

April’s US consumer price index (CPI) and producer price index (PPI) data both came in hotter than expected. The worrying detail in both was rising core services inflation — the sticky part of price growth that the Federal Reserve has struggled to wrestle down since the pandemic. Signs of spillover from energy into retail and wholesale transportation services warned that what started as a wartime price shock is becoming entrenched.

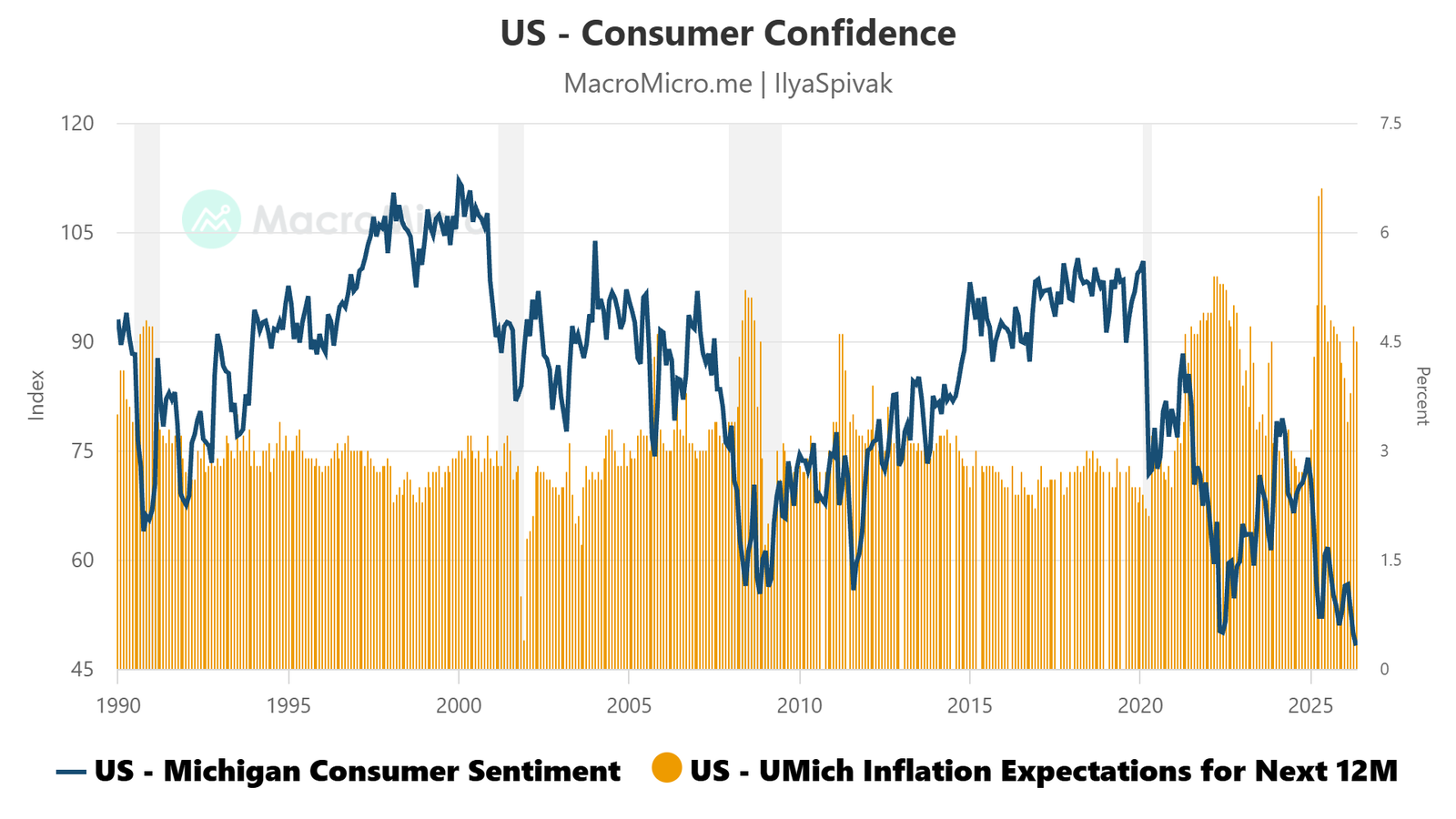

The April retail sales report then came in softer than the prior month, and with a worrying twist. A seemingly strong rise in March was mostly driven by a surge in gas station sales. That was a function of higher oil prices rather than stronger demand. April’s pullback in the same category came even as crude prices stayed firm, meaning the volume of gasoline sold probably fell. This warns that higher prices are starting to destroy demand. Tellingly, data from the University of Michigan (UofM) puts consumer confidence at its weakest since 1990, owing mostly to rising inflation expectations.

Markets now face three critical sentiment tests ahead

From here, an earnings report from Nvidia (NVDA) takes top billing. The chipmaker sits at the center of the AI buildout narrative, and with semiconductor names up more than 50% year-to-date while the rest of the market churns, anything underwhelming here could sour the mood well beyond the stock itself.

Minutes from May’s meeting of the Federal Open Market Committee (FOMC) are due the same day. With Kevin Warsh taking the helm as Fed Chair at the next meeting, the minutes may offer key insights on just how hawkish the rest of the policy-setting body has become. This has emerged as a critical variable given speculation that Warsh was nominated by President Donald Trump on the implicit promise of pushing for rate cuts.

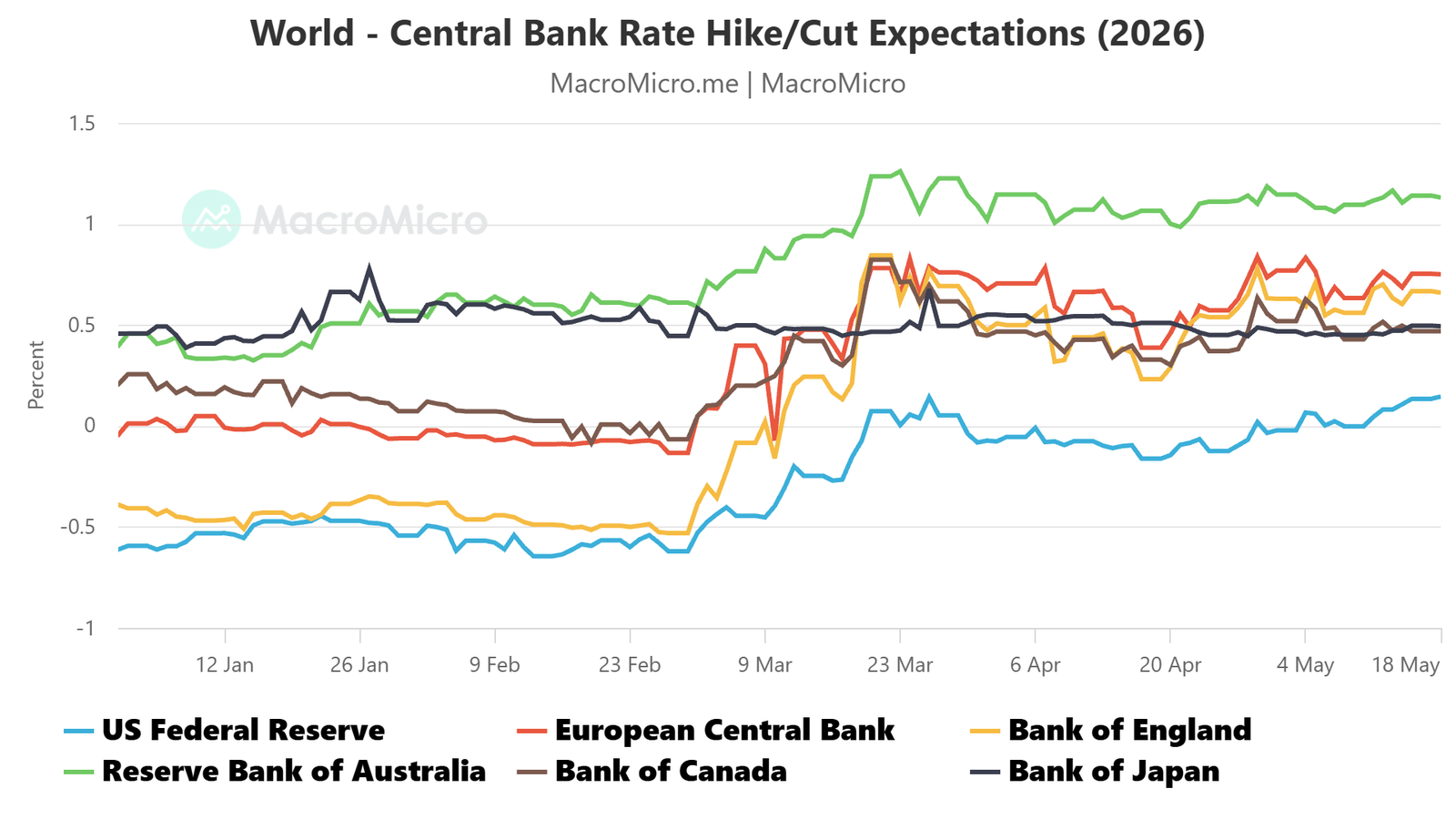

Markets are now pricing in about a 50/50 chance of a Fed rate hike before year-end, having been earmarked for two cuts before ethe US-Iran war began. A hawkish rethink is now on display for nearly all of the world’s top central banks. The European Central Bank (ECB) is fully priced for three hikes, the Bank of England (BOE) for two with near 50% odds of a third, and the Reserve Bank of Australia (RBA) has already delivered three of an expected four hikes, and with markets are now toying with the idea of a fifth.

The third test arrives with flash purchasing managers index (PMI) data covering the US, Eurozone, UK, Japan, and Australia from S&P Global. The numbers will offer a timely read on whether the global economy is already feeling the squeeze from higher prices and rising interest rates. Consensus calls favor relatively stable readings, but a downside surprise could land hard given how precarious the economic backdrop now appears.

Is the narrow stocks rally asking for too much?

First-quarter US gross domestic product (GDP) showed business investment contributing more to growth than consumption did, despite being five times smaller as a share of total output. That’s thanks to blistering capex spending aimed at building AI infrastructure. Data center builders faces the same headwinds as consumers however, from higher energy prices and fractured supply chains to surging borrowing costs.

Friday’s fireworks suggest the market is starting to do that math. The Cerebras IPO is past, the calendar is unfriendly, and three high-stakes catalysts arrive in quick succession. If Nvidia fails to impress, or the FOMC minutes set the stage for a clash between a hawkish committee and the incoming chair, or the flash PMIs reveal real cracks in global growth, the stock market melt-up could lose the support it has been running on for weeks.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

© copyright 2013 – 2026 tastylive, Inc.