Investors are in love with Goldilocks but should instead remain on the outlook for Disco Duck, according to a team of Wall Street quantitative strategists.

“Going back to the question of market macro regime, we believe that there is a risk of the narrative turning back from goldilocks towards something like 1970s stagflation, with significant implications for asset allocation,” wrote a team of J.P. Morgan analysts, led by closely followed strategist Marko Kolanovic, in a Wednesday note.

That 1970s scenario was a topic of discussion in the second half of last year, but was discarded in favor of “Goldilocks-type” or “just right” outcomes more recently, they said.

From the archives (October 2021): Why it’s wrong to compare today’s inflation surge to 1970s-style ‘stagflation’

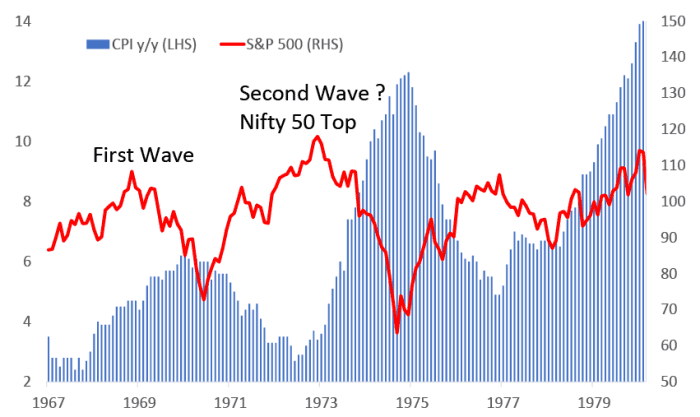

So what were the 1970s all about? Foremost was high inflation that came in three separate waves, with each timed in some way to geopolitical developments, the strategists observed.

Those included the Vietnam War as well as wars and revolutions in the Middle East. The latter were accompanied by oil embargoes that resulted in energy crises and shipping disruptions. The stage was also set for rising government budget deficits.

That should all sound somewhat familiar to investors today, they said, noting that equity markets were essentially flat from 1967 to 1980 in nominal terms, while bonds and credit outperformed significantly (see chart below).

“There are many similarities to the current times. We already had one wave of inflation, and questions started to appear whether a second wave can be avoided if policies and geopolitical developments stay on this course,” they wrote.

Also see: 1970s-style stagflation may be at risk of repeating itself, Deutsche Bank warns

The strategists see parallels between now and the 1970s geopolitical backdrop, noting three conflict zones: Eastern Europe, the Middle East and the South China Sea.

Related to those conflicts, investors have already witnessed one wave of an energy crisis, and the world is enduring a current round of shipping disruptions in the Red Sea.

The biggest risk by far revolves around tensions or a trade war with China that could have a much bigger impact on the global economy and would trigger a second wave of inflation and a market selloff, they said.

Meanwhile, fiscal deficits aren’t on a sustainable path.

It could all be setting up a reversion of the dynamic that prevailed from the late 1980s to the 2000s, in which a “peace dividend” from the end of the Cold War gets undone, turning into a macro backdrop characterized by a “conflict tax” or “conflict inflation,” the J.P. Morgan team said.

What would that mean for assets?

“If such a negative feedback loop were to take hold (as it did in the 1970s), investors would move out of equities and into fixed-income assets — i.e. seek to receive elevated yields that companies and governments need to pay to fund, rather than more elusive equity growth in a stagflationary regime,” wrote Kolanovic and company.

While stocks were flat from 1967 to 1980, bonds significantly outperformed, with yields averaging above 7%, they noted — which meant that any yield pickup, such as that provided by private credit, would make a huge difference to long-term portfolio performance.

Investors don’t appear in the mood so far to revisit the 1970s. Stocks have rallied into 2024, with the S&P 500 SPX passing the 5,000 milestone, while the Dow Jones Industrial Average DJIA has scored a string of record highs.

Stocks eked out gains Wednesday as investors weighed the minutes of the Federal Reserve’s policy meeting in January.

Stock Market Today: Dow, S&P 500 erase losses before bell as market weighs Fed minutes, awaits Nvidia results