With the 4th of July around the corner, it’s worth remembering that sometimes the loudest, brightest things typically fade at some point. In financial markets, we’ve seen the most hyped segment is also this year’s worst performer. But here’s why that might actually be a good thing.

The loudest stock in the room

On June 12, a crowd gathered outside the Nasdaq in Times Square to watch a single stock start trading, and for a few hours it had the financial world’s full attention. SpaceX priced its IPO at $135 a share, opened higher, and finished its first day up about 19%, at $161. It was the largest IPO in history, valuing the company near $1.77 trillion. Four days later the stock touched $225 only to fall into the $150s down ~33% from that high in only two weeks.

If that round trip gives you a queasy, tech-bubble like feeling, you’re not the only one. The word “bubble” is everywhere again, both for the market as a whole and for AI in particular. Other events in June didn’t help with the nerves either as a ceasefire with Iran fell apart almost as fast as it was announced, and Kevin Warsh ran his first meeting as the new Fed chair, without forward guidance. Markets, on cue, went along for the ride as the S&P 500 and tech-heavy Nasdaq were down 4% and 6% mid-month, before clawing that back to finish flat on the month.

Is the loudest part of the market also the riskiest?

The honest answer about timing a bubble is that nobody knows, and anyone who tells you they can call the top in advance is guessing. People have been calling for a bubble since the pandemic (some even since the 2008 financial crises), and stock markets kept climbing anyway.

What we do know is that the math doesn’t rhyme with 2000. A price-to-earnings ratio (aka what you have to pay for each dollar of a company’s profits) is the most widely cited gauge of how cheap or expensive stocks are relative to their peers. At the peak of the dot-com bubble, the Nasdaq 100 traded around 58 times forward earnings. Today it’s closer to 25. And the biggest difference, a lot of the 2000 tech darlings had no earnings at all. Today’s leaders make real money, and plenty of it, even before AI was in focus.

That doesn’t mean there’s no froth at all. SpaceX is a great example. A company that’s never turned a profit, trading at $1.77 trillion, is not exactly priced to next year’s earnings. That’s real speculation. It’s just not the entire market. And if you’re worried you already own this thing once it lands in the broad index funds that track it, SpaceX pencils in around 0.1% of a broad index fund which is a rounding error, not something to lose sleep over.

Most of the bubble worry also centers on how much Big Tech is spending. Microsoft, Amazon, Alphabet, and Meta are on track to lay out roughly $725 billion on capital expenditures (the money a company spends building things like data centers). And that number is up 77% from last year, with analysts pointing toward $1 trillion in 2027. That spending is real enough to dent free cash flow and the fear is reasonable. What if all that money never pays off?

The piece I think that fear leaves out is the demand side. The whole worry is about supply and the building of it all. But when was the last time you, or the company you work for, used less AI than before? Adoption has only been climbing as the quality of the technology continues to improve. The revenue may lag the spending for a while, but “we’ll use less of this at some point” doesn’t seem in sight.

It’s also worth adding that this year’s stock market gains have also been led by earnings, not by investors simply agreeing to pay higher multiples. Rallies built on actual profits tend to be far more durable than rallies built on enthusiasm alone.

The boring stuff is outperforming

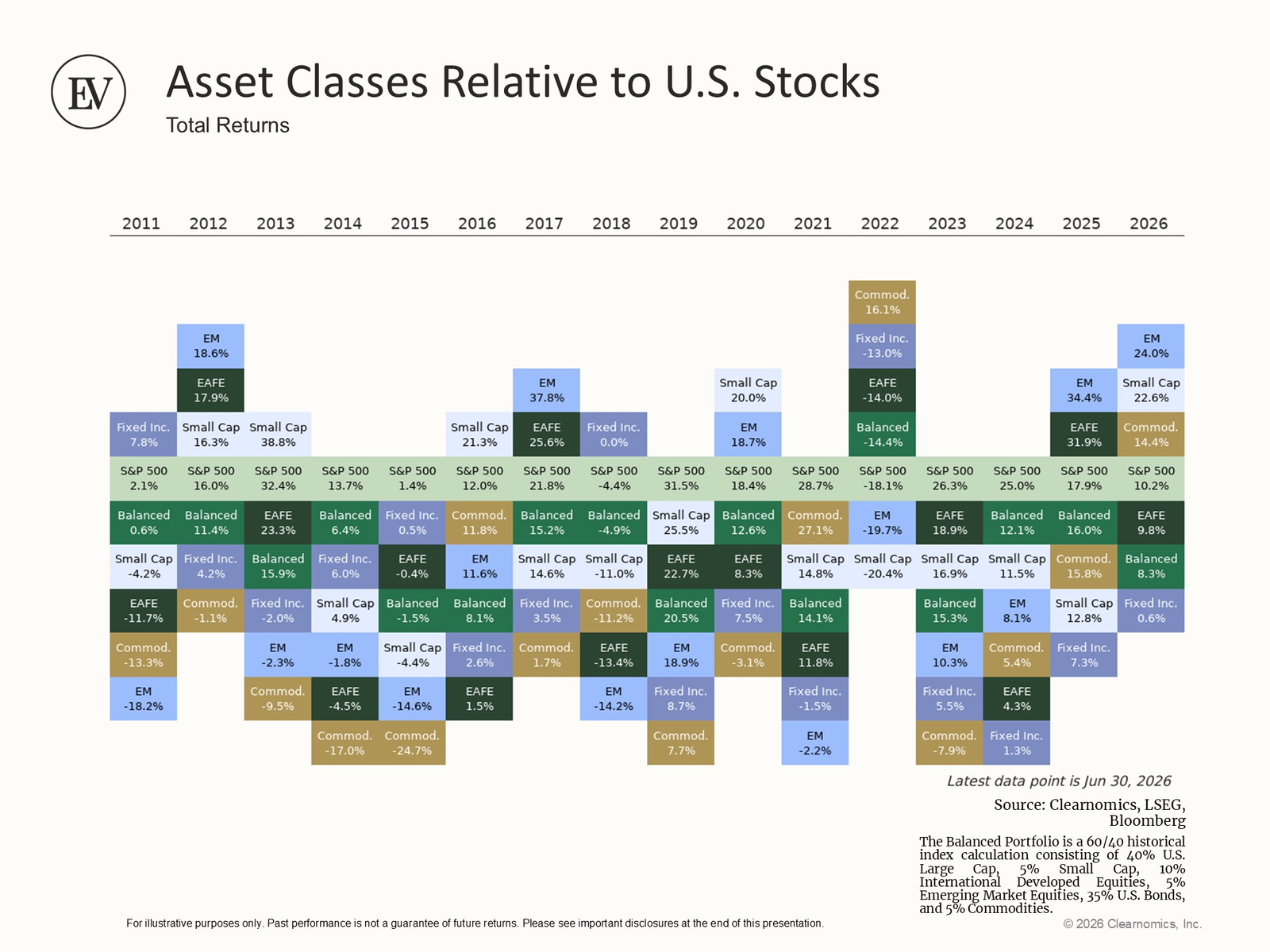

This is another part all the bubble talk misses … every bit of the attention is on AI and tech. Yet those have been the laggards this year. Through June, Emerging Markets are up 24%, US Small Caps 23%, and US Large Cap Value 15%. Meanwhile, the S&P 500 is up 10%. And the Magnificent 7 stocks, the large tech everyone’s worried is in a bubble, is down -3%.

The loudest, most hyped, part of the market is its worst performer this year. The quiet, boring stuff you typically never hear about is climbing. That broadening matters more than it might seem. Market breadth measures how many stocks are participating in a rally versus a select few carrying it. A bubble typically shows a narrowing market, not a broadening one. And stronger breadth is generally viewed as a healthier market environment as the market becomes less reliant on fewer stocks or sectors.

Turning down the volume

Think back to that crowd outside the Nasdaq. The stock everyone gathered to watch gave back almost a third of its value in two weeks, while the quiet, unglamorous corners you never hear about (emerging markets, small caps, value) did the heavy lifting.

Is this a bubble? We don’t know, and neither does anyone claiming to. But you don’t need to call it. A diversified portfolio already owns a piece of whatever wins, steady enough to tune out this month’s noise, and the loudest stock in the room becomes what it should be … a small part of a much bigger picture.