Stock markets cheer even as the US economy leans on a data center boom that is already running into trouble

- US Q1 GDP growth rose to 2%, with business investment doing more of the work than the consumer

- AI “hyperscalers” are touting huge capex plans even as energy supply, tariffs, and politics push back

- The ECB and BOE joined the Fed in a hawkish chorus as the Iran war’s inflation pulse spreads abroad

Stocks are surging into month-end as the rest of the major asset classes continue to trade the US-Iran war. The first-quarter US GDP report gave equity bulls something to celebrate, but the composition raises an uncomfortable question: can the data center buildout carry the economy if the consumer keeps slowing and the inflation pulse keeps spreading?

Stocks remain alone, with conviction still fading

The bellwether S&P 500 is at fresh record highs, but the technical issues flagged at the start of the week are still glaring. Volumes collapsed precisely as the rebound from the US-Iran wartime selloff crossed back into prices’ pre-war range. The relative strength index (RSI) momentum gauge shows negative divergence, where prices set higher highs, but the indicator doesn’t. This warns that the upward thrust may be running out of steam.

Crude oil is back near the top of its wartime range. Treasury bond prices are sharply lower as yields push higher with central banks reacting to the energy shock. Gold is selling off as rising yields and a broadly stronger US dollar make non-interest-bearing and anti-fiat assets less attractive.

The greenback was knocked back as Japanese authorities intervened to prop up the yen. A sharp drop in the USD/JPY echoed as broader dollar weakness across global markets, but this seems like a one-off, at least for now.

Besides stocks, bitcoin is the lone major asset besides stocks that seems unbothered by “war trade” dynamics.

US Q1 GDP looks better than it really is

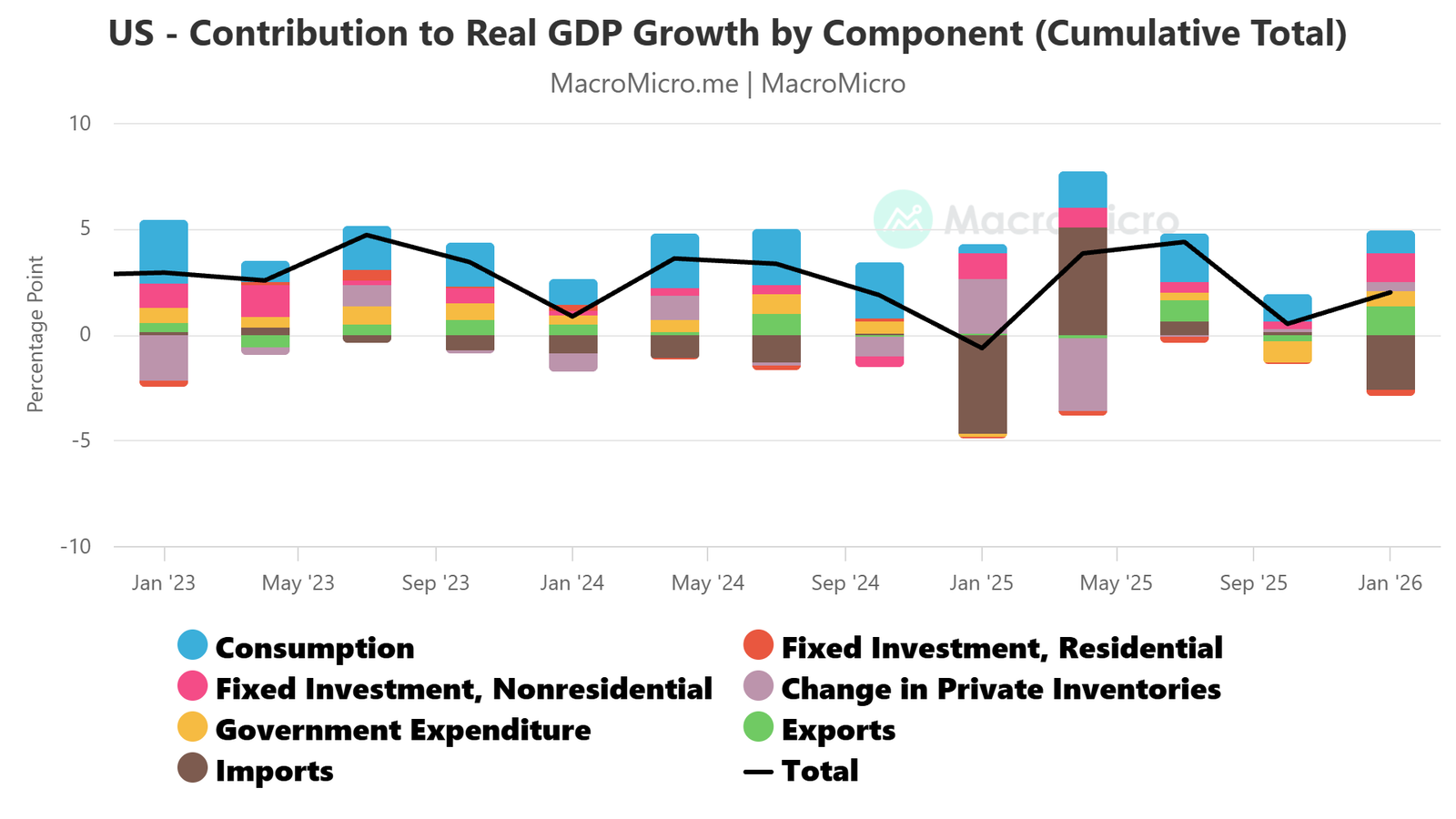

First-quarter US gross domestic product (GDP) data showed the economy grew at an annualized rate of 2%, up from 0.5% in the last three months of 2025. This improvement is real but flattered by base effects: performance in the fourth quarter was depressed by a government shutdown that has since been resolved. The second- and third-quarter trend was closer to 4%. This means that the economy is only about halfway back to where it was pre-shutdown.

More telling still is growth’s composition. Fixed nonresidential investment contributed 1.39 percentage points (ppt) to the 2% headline figure, edging out consumption at 1.08ppt. Government spending swung positive after the shutdown, while net exports shaved off 1.3ppt as imports outpaced exports by a meaty margin.

Most strikingly, business investment is surging while consumption has decelerated from its peak in the third quarter. The driver is artificial intelligence (AI) data center construction. Earnings reports from AI “hyperscaler” companies produced mixed results this week — Alphabet (GOOG) rallied, Meta (META) got shellacked — but all of the major players announced lavish capex plans.

The data center boom is hitting real constraints

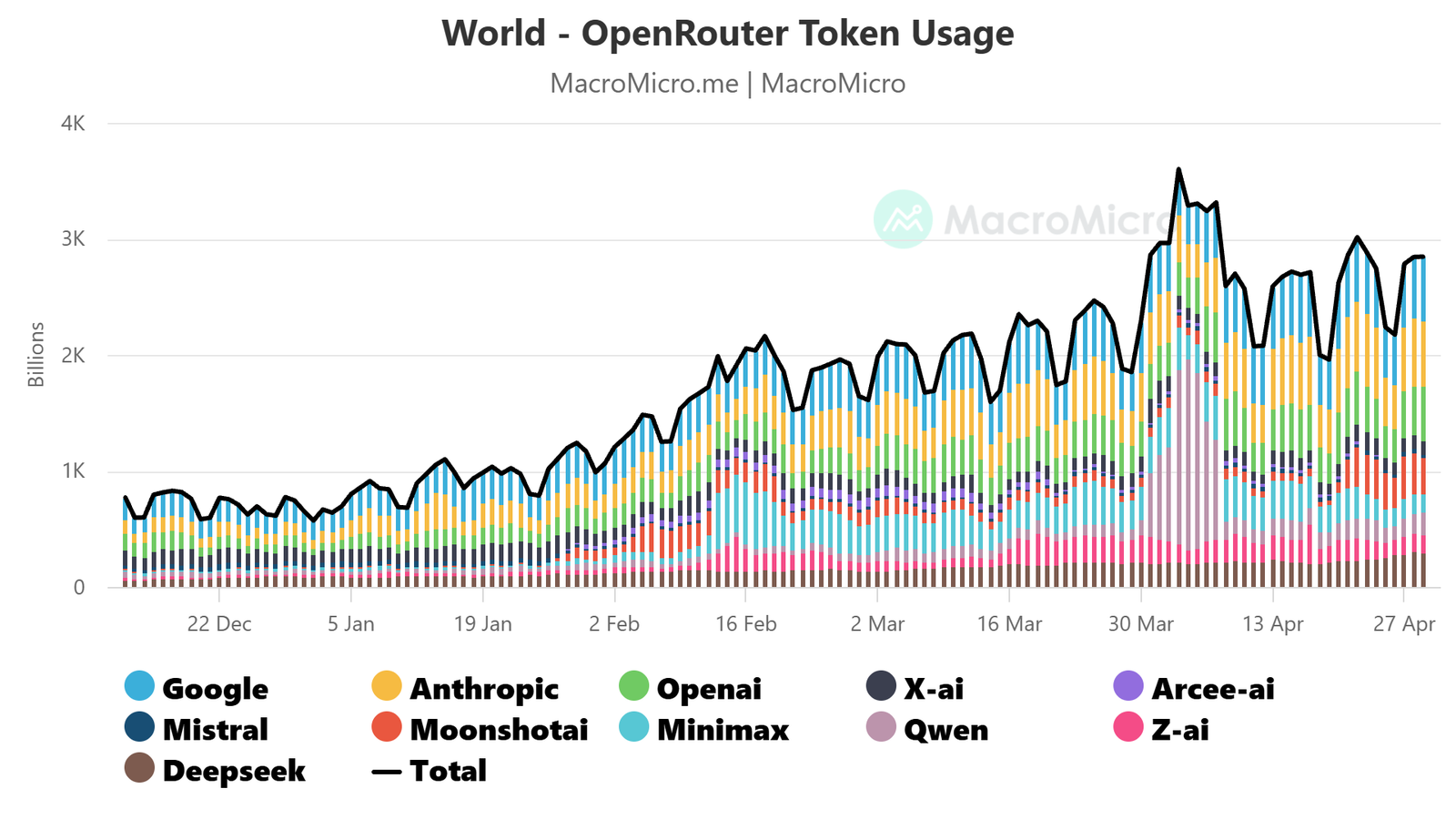

Demand justifies the big-splash outlays. Traffic to AI tools is climbing, OpenRouter token usage is accelerating, and capacity is the binding constraint. Anthropic has imposed peak-time usage limits and OpenAI has shut down its Sora video generation tool to redirect compute resources elsewhere.

The buildout is colliding with the real economy however. Energy prices are rising. At least ten US states are weighing moratoriums on data center building and the governor of Maine — who vetoed one such bill — has been driven out of her Senate race. Tariffs are amplifying pressure on already fragmented supply chains hamstrung by the closing of the Strait of Hormuz.

Capex plans are huge, but whether they can be realized as advertised in practice seems to be another matter.

Inflation is broadening as central banks turn hawkish

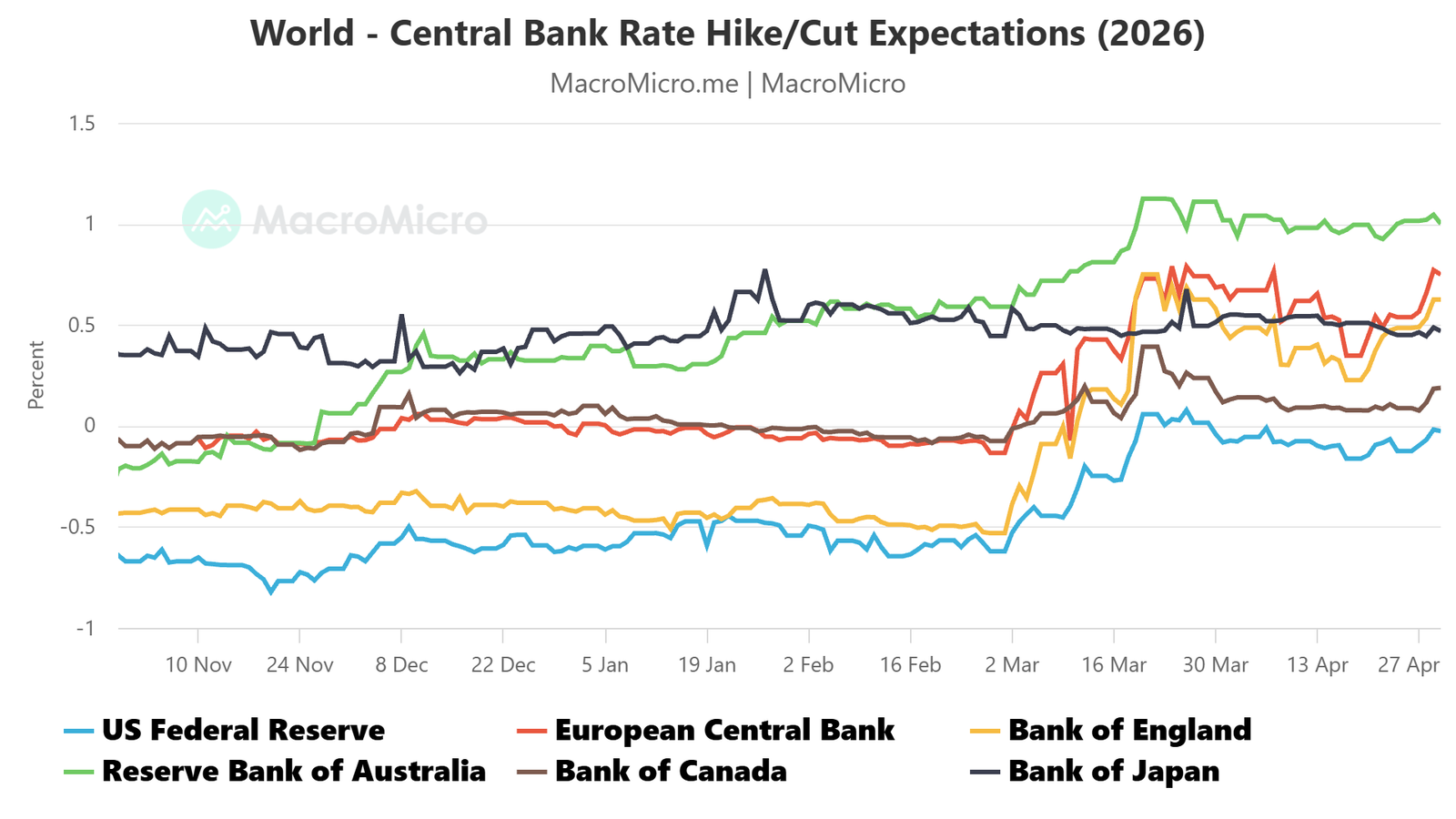

The Federal Reserve, the European Central Bank (ECB), and the Bank of England (BOE) all delivered hawkish messages this week. In the US, core goods, services, and housing prices are posting the largest gains in months. None of that includes energy — and with the typical one-month lag from crude into headline US consumer price index (CPI), only the early-year run-up has shown up so far. The bigger war-linked spike is still in the pipeline. The 10-year breakeven inflation rate is back to mid-2025 levels.

Markets now price in 75 basis points (bps) of ECB hikes by year-end and at least 50bps from the BOE. Even the Bank of Canada (BOC) is now favored to raise rates at least once in 2026. Fed funds futures imply a hold for the US central bank this year, but the priced-in probability of a hike outweighs that of a cut at every meeting through October 2027.

The vicious cycle the stock market is ignoring

Pull this together and the longer-term picture looks ominous. The consumer is decelerating with no near-term reprieve. Meanwhile, the data center buildout doing the heavy lifting on growth is running into energy, political, and supply chain limits. If the hyperscalers force through spending anyway, the result is likely to be more inflation and still higher rates — a vicious cycle.

Other markets seem worried about just such a scenario, even as stocks blissfully ignore it. That makes overall risk sentiment appear vulnerable. With the earnings report from Apple (AAPL) seemingly passing without major incident and closing the book on mega-cap tech results until Nvidia (NVDA) reports on May 20, the mood on Wall Street may be ripe for a change.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

© copyright 2013 – 2026 tastylive, Inc.