The CAPE ratio is flashing a warning that, in over a century of stock market history, has only shown up once before: near the top of the dot-com bubble.

With the S&P 500 (^GSPC +1.18%) and Nasdaq Composite indexes both near record highs, it stands to reason to ask, should I be worried? Here’s what you need to know.

What is the CAPE ratio?

CAPE stands for the cyclically adjusted price-to-earnings ratio. It’s basically a smoothed-out version of the regular price-to-earnings (P/E) ratio — a standard valuation metric for a stock — but applied to the whole market. It takes the price of the S&P 500 and divides it by the average of its inflation-adjusted earnings over the past 10 years.

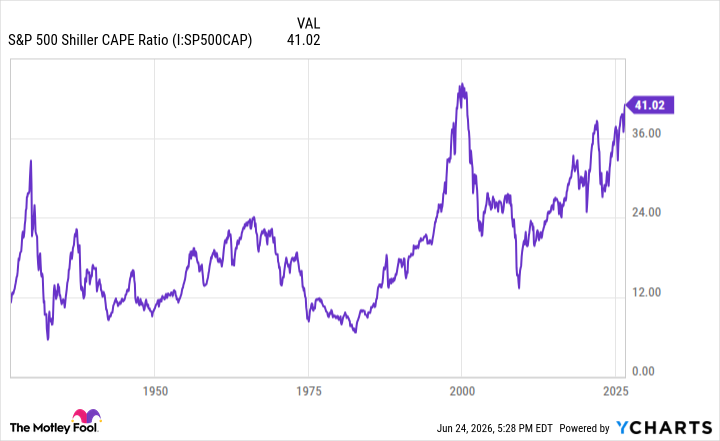

The decade-long average helps smooth things out and remove the noise. It gives you a cleaner read on what investors are really paying. When the ratio runs high, the market is expensive relative to what companies have actually earned. The historical average sits around 17, and right now we’re north of 40 — more than double the long-run norm.

We’ve only been here once before

The only other time the CAPE crossed 40 was in 1999, right at the top of the dot-com bubble. The S&P 500 had roughly tripled over the prior five years, fueled by enthusiasm for internet stocks that mirrors today’s enthusiasm for all things artificial intelligence (AI).

Take a look at the CAPE over the last 100 years.

S&P 500 Shiller CAPE Ratio data by YCharts

Why this time could be different

It might be a mistake to assume this ends the same way, however. There’s certainly a good argument for why this is not the same market.

The dot-com highs were driven by speculation on companies that were, in many cases, barely businesses. This was the era of Pets.com and eToys — stocks were sent soaring based more on a concept than any fundamentals.

Today, the market is dominated by tech giants with massive earnings. Apple, Microsoft, Nvidia, Alphabet, and Amazon have the balance sheets and income statements to back up their stock prices.

Earnings have been soaring, and it’s not hard to see the CAPE retreating to more reasonable levels, not through a crash in stock prices, but the steady rise of the net income these companies book.

Why today’s earnings might not be as solid as they look

While there’s merit to this argument, I’m inclined to push back on it for a key reason: Today’s earnings might not be as “real” as they seem. This is because of a pretty straightforward accounting quirk that many investors miss but is critical to understand.

The bulk of the money sloshing around in the AI economy, driving the market, comes from the capital expenditures of the big tech hyperscalers like Alphabet and Microsoft. This money flows out immediately, boosting revenue and earnings across the entire ecosystem, but it isn’t counted against the hyperscalers’ own earnings up front. It gets spread out over time.

Image source: Getty Images.

This leads to a lag in which the benefits of that spending are reflected in the CAPE, while the costs show up later. To be sure, there’s nothing nefarious going on here; it’s just the way accounting works. But when this window closes, the CAPE could suddenly look even more extreme. And that could be coming soon.

What investors should do now?

OK, so where does this leave us? Well, you definitely shouldn’t go running for the hills. It matters that the CAPE is at historic levels, but it’s not some crystal ball. It guarantees nothing — most of all, timing. The truth is, while the CAPE is now the second-highest it’s ever been, it’s been in “danger” territory for more than a decade. You would have missed out on quite a bit of growth had you sat in cash when the CAPE passed 30 in 2017.

It’s a cliche, yes, but it’s not a tired one, in my opinion: Time in the market beats timing the market. Patient investing over the long term is always the winning formula.

With that said, now is not the time to chase high-flying growth stocks, nor is it the time to be all in on companies with mind-numbing valuations based on the promise of future revenue. Companies that will do well with or without an AI revolution are a great bet.