The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines amid weak trade data from China, highlighting global economic uncertainties. In such a climate, identifying stocks that may be trading below their estimated value can offer potential opportunities for investors seeking to navigate these turbulent times effectively.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

|

Name |

Current Price |

Fair Value (Est) |

Discount (Est) |

|

On the Beach Group (LSE:OTB) |

£1.546 |

£3.09 |

50% |

|

AstraZeneca (LSE:AZN) |

£119.46 |

£237.51 |

49.7% |

|

S&U (LSE:SUS) |

£19.20 |

£36.51 |

47.4% |

|

Watches of Switzerland Group (LSE:WOSG) |

£4.50 |

£8.51 |

47.1% |

|

Redcentric (AIM:RCN) |

£1.20 |

£2.39 |

49.8% |

|

Gulf Keystone Petroleum (LSE:GKP) |

£1.271 |

£2.47 |

48.6% |

|

Ferrexpo (LSE:FXPO) |

£0.528 |

£0.98 |

45.9% |

|

Foxtons Group (LSE:FOXT) |

£0.618 |

£1.19 |

48.2% |

|

St. James’s Place (LSE:STJ) |

£8.76 |

£16.38 |

46.5% |

|

Genel Energy (LSE:GENL) |

£0.803 |

£1.53 |

47.5% |

Here’s a peek at a few of the choices from the screener.

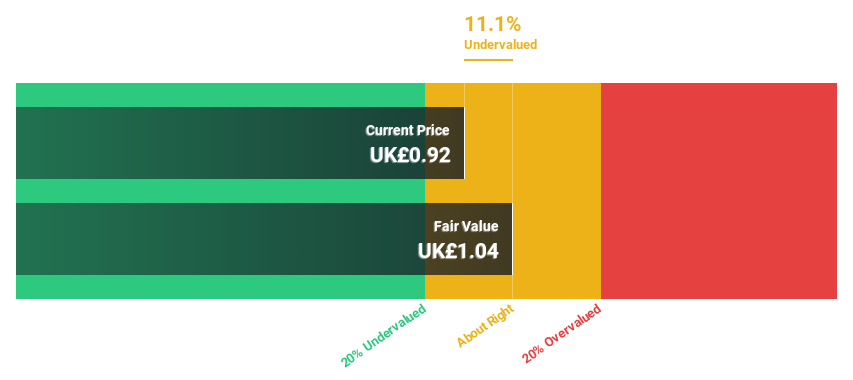

Victorian Plumbing Group

Overview: Victorian Plumbing Group plc is an online retailer specializing in bathroom products and accessories in the United Kingdom, with a market capitalization of £359.90 million.

Operations: The company generates revenue of £282.90 million from its online retail operations focused on bathroom products and accessories in the UK.

Estimated Discount To Fair Value: 43.8%

Victorian Plumbing Group appears undervalued based on discounted cash flow analysis, trading at £1.11, significantly below the estimated fair value of £1.97. Despite recent insider selling, the company’s earnings are forecast to grow at a robust 36.2% annually, outpacing the UK market’s growth rate of 14.1%. The stock is priced attractively at 43.8% below its fair value estimate, with anticipated revenue growth of 9.9% per year exceeding market expectations.

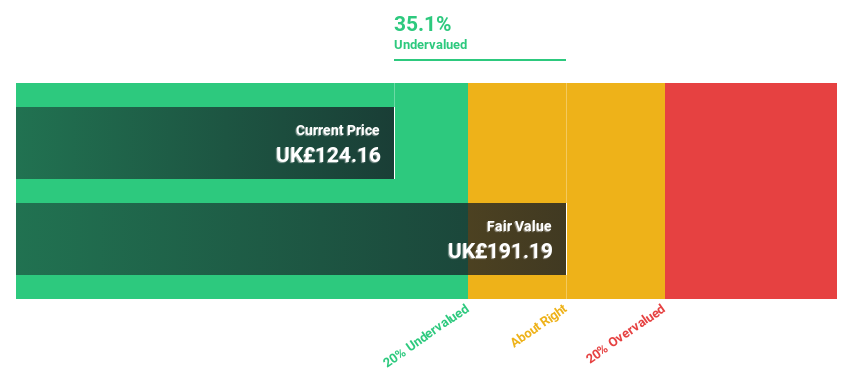

AstraZeneca

Overview: AstraZeneca PLC is a biopharmaceutical company that specializes in the discovery, development, manufacture, and commercialization of prescription medicines, with a market cap of approximately £185.20 billion.

Operations: The company’s revenue primarily comes from its biopharmaceuticals segment, which generated $49.13 billion.

Estimated Discount To Fair Value: 49.7%

AstraZeneca is trading at £119.46, significantly below its estimated fair value of £237.51, suggesting it may be undervalued based on discounted cash flow analysis. Despite a high debt level and earnings impacted by large one-off items, the company’s earnings are forecast to grow at 16.53% annually, outpacing the UK market’s growth rate of 14.1%. Recent positive trial results and strategic collaborations could enhance future revenue streams and bolster financial performance.

John Wood Group

Overview: John Wood Group PLC provides consulting, project management, and engineering solutions to the energy and built environment sectors globally, with a market cap of £927.42 million.

Operations: The company’s revenue is derived from four main segments: Projects ($2.27 billion), Consulting ($737.30 million), Operations ($2.58 billion), and Investment Services ($174 million).

Estimated Discount To Fair Value: 35.4%

John Wood Group is trading at £1.35, significantly below its estimated fair value of £2.09, indicating it may be undervalued based on discounted cash flows. Despite recent net losses and volatile share price movements, the company is expected to achieve profitability within three years with earnings growth forecasted at 96.78% annually. The board’s rejection of acquisition offers underscores confidence in future prospects and anticipated significant cash flow generation in 2025 amidst moderate revenue growth projections.

Make It Happen

-

Delve into our full catalog of 60 Undervalued UK Stocks Based On Cash Flows here.

-

Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

-

Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

-

Explore high-performing small cap companies that haven’t yet garnered significant analyst attention.

-

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

-

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include AIM:VIC LSE:AZN and LSE:WG..

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com