Falling oil and steadier bonds hint the rate scare is fading, which ought to cheer stocks — yet they won’t budge. With a US jobs report on deck and real wages turning negative, the market may be bracing for the wrong kind of cooldown.

- The S&P 500 is churning near the middle of its range, with the makings of a rare diamond-top pattern taking shape

- Workers’ real earnings have turned negative as inflation finally outpaces wage growth

- Friday’s payrolls report will show whether a softening economy means benign disinflation or something more menacing

The bellwether S&P 500 rose this week and still went nowhere, churning near the middle of the range that has boxed it in since May. The chart may be tracing out a diamond top — an uncommon reversal pattern that, if it breaks, would project a decline toward roughly 6900. There is no break yet, only chop. What makes the stall telling is that the backdrop ought to be helping stocks, not stalling them.

The rate scare is fading, so why won’t stocks rally?

Across the assets that traded the US-Iran war, the inflation fear is visibly draining. Crude oil has erased almost the entire geopolitical premium built up since the conflict began in late February, with the ceasefire broadly holding. Treasury bonds, hammered lower through the war as yields climbed, are trying to base and even overturn their downtrend. Gold’s long selloff is losing vigor, its lower lows no longer confirmed by momentum. Together they suggest interest rates may not need to be as punishing as markets assumed at the height of the war scare — which should be a gift to equities.

Instead, stocks sit frozen, and so does the US dollar, refusing to fall even as its yield advantage softens. That reluctance is itself a warning. The greenback plays two roles — it rewards the holder when the Fed looks relatively hawkish, and it serves as the ultimate cash haven, settling close to 90% of global transactions. That sentiment barometers like stocks and the dollar refuse to relax even as the rate threat recedes suggests traders are finding something new to be worried about.

Beneath the manufacturing boom, demand is cooling

The something else is the consumer, and this week’s manufacturing data hinted at the strain. June’s Institute for Supply Management (ISM) survey came in a touch soft at 53.3 against a forecast of 54.0. That’s still a booming reading – the second highest in four years, after the prior month’s blistering result – powered by the input stockpiling behind the artificial intelligence (AI) buildout. But the internals told a quieter story: order backlogs flattened, new orders slowed, production eased, and supplier deliveries quickened — the fingerprints of demand that is starting to soften. Most striking of all, factory employment kept shrinking even as output surged. The boom, in other words, is not creating jobs.

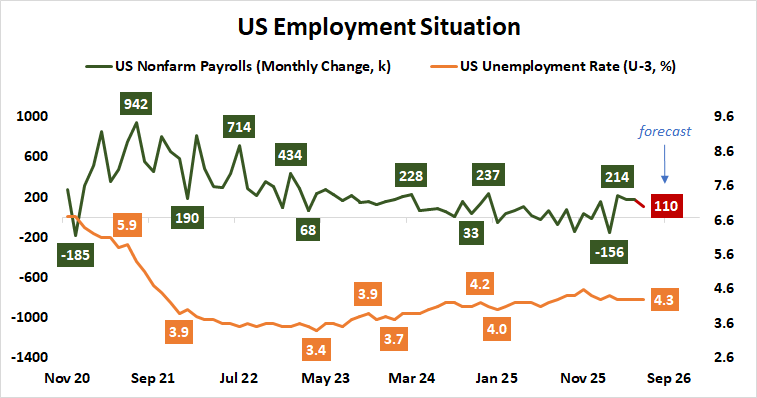

The number that matters: paychecks are losing to prices

That sets up Friday’s June payrolls report as the pivotal read of a holiday-shortened week. Hiring is expected to slow to 110,000, a clear downshift from the roughly 188,000 monthly average of the prior three months. The headline matters, but the deeper signal sits in wages. For three years, pay growth outran inflation, a steady tailwind that kept consumers spending. That tailwind has just reversed: average hourly earnings, seen at 3.5% year-on-year, now trail an inflation rate running north of 4%. Real earnings have turned negative, and households are losing ground for the first time in three years.

This is where the growth story turns menacing. First-quarter gross domestic product (GDP) rose 2.1%, but the muscle came from business investment — barely 15% of the economy, growing above a 10% annualized clip — while consumption, five times larger at 68% of GDP, contributed almost nothing by comparison. Wringing growth from so small an engine means running it hot enough to throw off inflation, and that inflation settles in core services, precisely where household spend is concentrated. So, the very boom animating the economy is eroding the paychecks that are supposed to carry it. With real wages now negative, that squeeze has a number on it.

Benign cooldown or demand destruction?

Markets have penciled in one more Fed rate hike — futures put September odds near 77% and October at almost 99% — followed by a long hold. But if the payrolls data shows the consumer buckling, that framing unravels, because the inflation-driven case for higher rates only holds while the economy is still growing. The tentative reversals stirring in bonds and gold would then gather force, as the market concludes rates have less room to rise than feared. Europe and Australia offer the cautionary template: booming factories catching the AI wave, yet economies sliding into contraction as inflation guts their far larger service sectors.

The decisive question is what kind of cooldown this is. If disinflation arrives gently, stocks may yet find their footing. If instead it comes as outright demand destruction — the consumer cracking under prices that outpace pay — the path of least resistance for equities is down, toward that diamond-top target. The dollar would likely climb in that scenario even as US rates lose their shine, because a genuine growth scare sends investors scrambling for the deepest pool of cash on the planet. Friday’s report will not settle it outright, but it will show whether the consumer is bending or breaking — and the market, frozen and watchful, clearly suspects the answer is the darker one.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

© copyright 2013 – 2026 tastylive, Inc.