- On September 22, 2025, Citigroup initiated coverage on Ryder System with a new rating and highlighted the company’s tech-enabled logistics services and recent dividend hike, shortly before Ryder was scheduled to present at MOVE America 2025 in Detroit.

- Ryder’s strengthened analyst attention and focus on shareholder returns come as the transportation sector faces ongoing supply chain challenges and evolving logistics demands.

- Now, we’ll assess how Ryder’s analyst upgrades and innovation focus may influence its investment narrative and future growth outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Ryder System Investment Narrative Recap

To be a Ryder System shareholder, you must believe in the resilience of U.S.-centric industrial logistics and Ryder’s ability to execute in a challenging, tech-driven transportation environment. While Citigroup’s new coverage and Ryder’s upcoming MOVE America 2025 presentation may lift sentiment and near-term attention, these events do not materially change the key short-term catalyst: contract wins in supply chain and dedicated fleet businesses. The biggest risk remains prolonged freight market softness, which could pressure recurring revenue and margin stability.

Among the recent announcements, Ryder’s 12% dividend hike stands out, reinforcing the company’s emphasis on rewarding shareholders even as the transportation sector faces headwinds. Analyst upgrades following this move have spotlighted Ryder’s financial strength and cash generation, both of which are important to support expansion in tech-enabled logistics, a core area of interest for investors tracking the impact of supply chain digitization.

However, despite increasing analyst optimism, investors should be mindful of persistent freight market volatility and the risk that contract volumes may not rebound as quickly as expected if economic uncertainty lingers…

Read the full narrative on Ryder System (it’s free!)

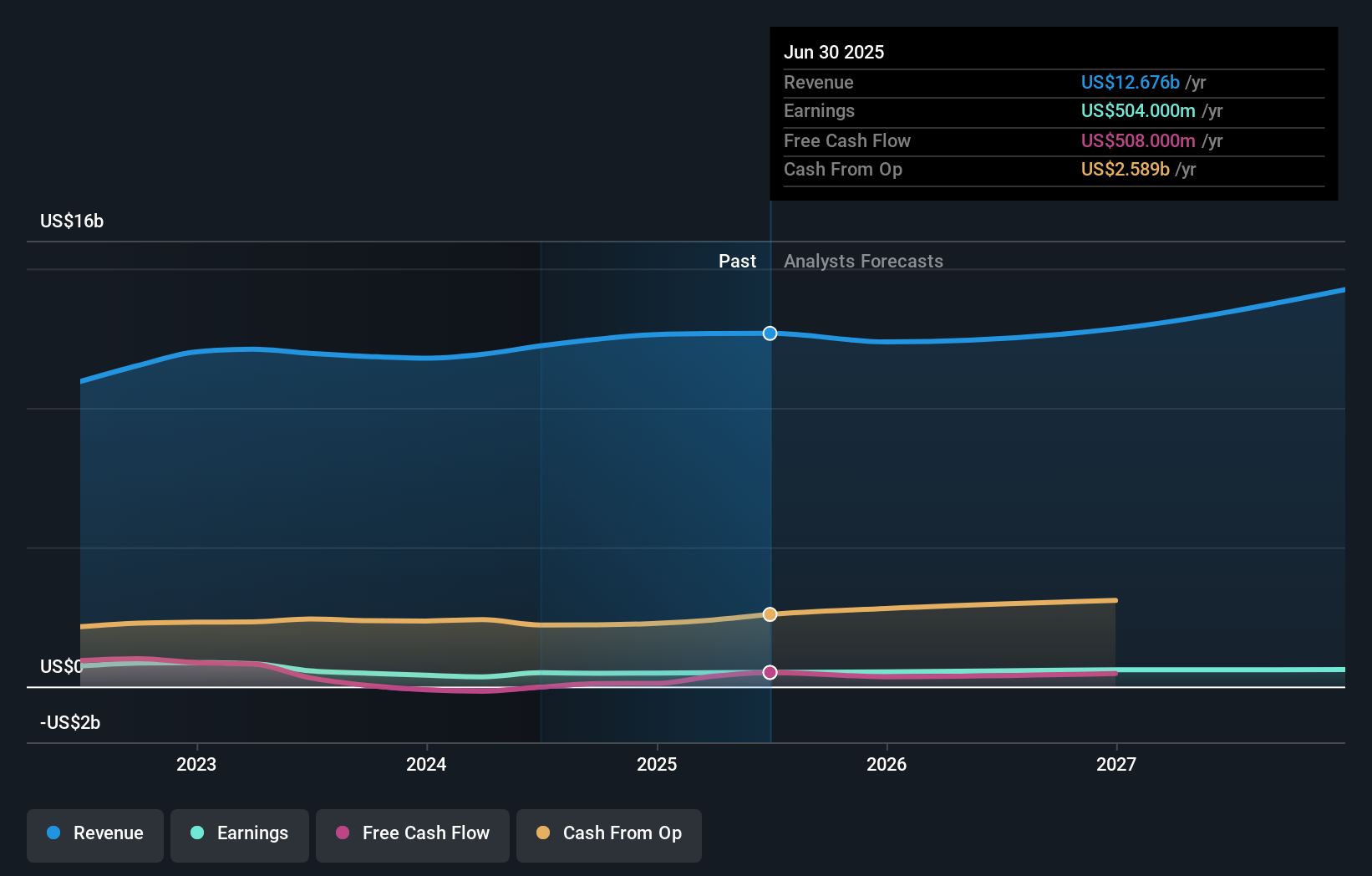

Ryder System’s outlook forecasts $14.4 billion in revenue and $657.9 million in earnings by 2028. To achieve this, analysts expect revenue to grow at 4.4% annually and earnings to rise by $153.9 million from $504.0 million today.

Uncover how Ryder System’s forecasts yield a $196.56 fair value, a 5% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members put Ryder’s fair value between US$196.56 and US$218.77, based on 2 independent forecasts. With conflicting views on contract volumes and used vehicle pricing, these contrasting investor opinions highlight the importance of understanding sector risks before forming your own expectations.

Explore 2 other fair value estimates on Ryder System – why the stock might be worth as much as 17% more than the current price!

Build Your Own Ryder System Narrative

Disagree with existing narratives? Create your own in under 3 minutes – extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ryder System research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ryder System research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Ryder System’s overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump’s tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com