Markets want to hear the Fed is ready to bail them out if things get rocky, even if it balks at rate cuts now.

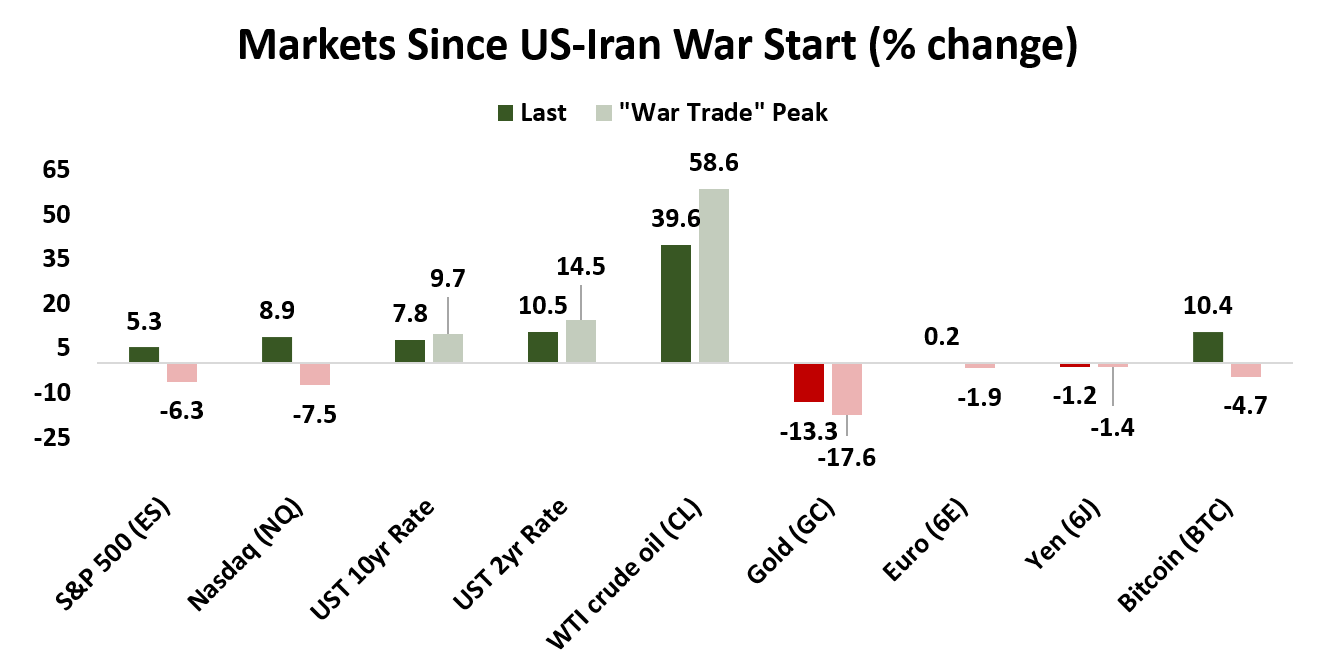

- Stocks are on an island as bonds, gold, and the dollar continue the “war trade”

- Core goods, services, and housing inflation were rising before oil prices spiked

- Four of the Mag7 tech firms will report earnings as conviction seems to fade

Markets are meandering ahead of a wall of event risk over the next 24 hours. The Federal Reserve policy announcement leads off, followed by earnings from four of the Magnificent Seven big tech names.

Stocks are alone, and conviction is fading

The setup seems telling. The S&P 500 is losing yesterday’s attempt at an upside breakout, and the divergences flagged earlier this week look more acute.

Volumes have faded throughout the rebound from the US-Iran wartime selloff, with yesterday’s session marking the lowest volume in the front-month E-mini S&P 500 (ES) futures contract since the Easter Monday lull. Tellingly, today’s pullback is happening on heavier participation than yesterday’s push higher.

The relative strength index (RSI) momentum indicator is also showing negative divergence: price is setting higher highs while the RSI is not. The capacity for prices to close higher relative to lower is fading even as new nominal records are set. That is not always a precursor to a reversal, but it often is.

And stocks are alone in the melt-up. Most other major markets are still trading the war.

Bonds, gold, and the dollar are still trading the war

Crude oil sits near the middle of its wartime range, around $100 a barrel and nearly 40% above pre-war levels. Treasury bond prices have resumed sliding, sending yields creeping higher again. The 10-year breakeven inflation rate is at its highest since mid-2025, fully erasing the disinflation that prompted the Fed to begin cutting rates last year.

The US dollar has retraced only about half its wartime gains and is starting to edge higher. Gold is leaking lower as rising yields and a stronger greenback make non-interest-bearing and anti-fiat assets less attractive.

Besides stocks, bitcoin is also in the green, but it seems to be marching to the beat of its own drum rather than war-related capital flows.

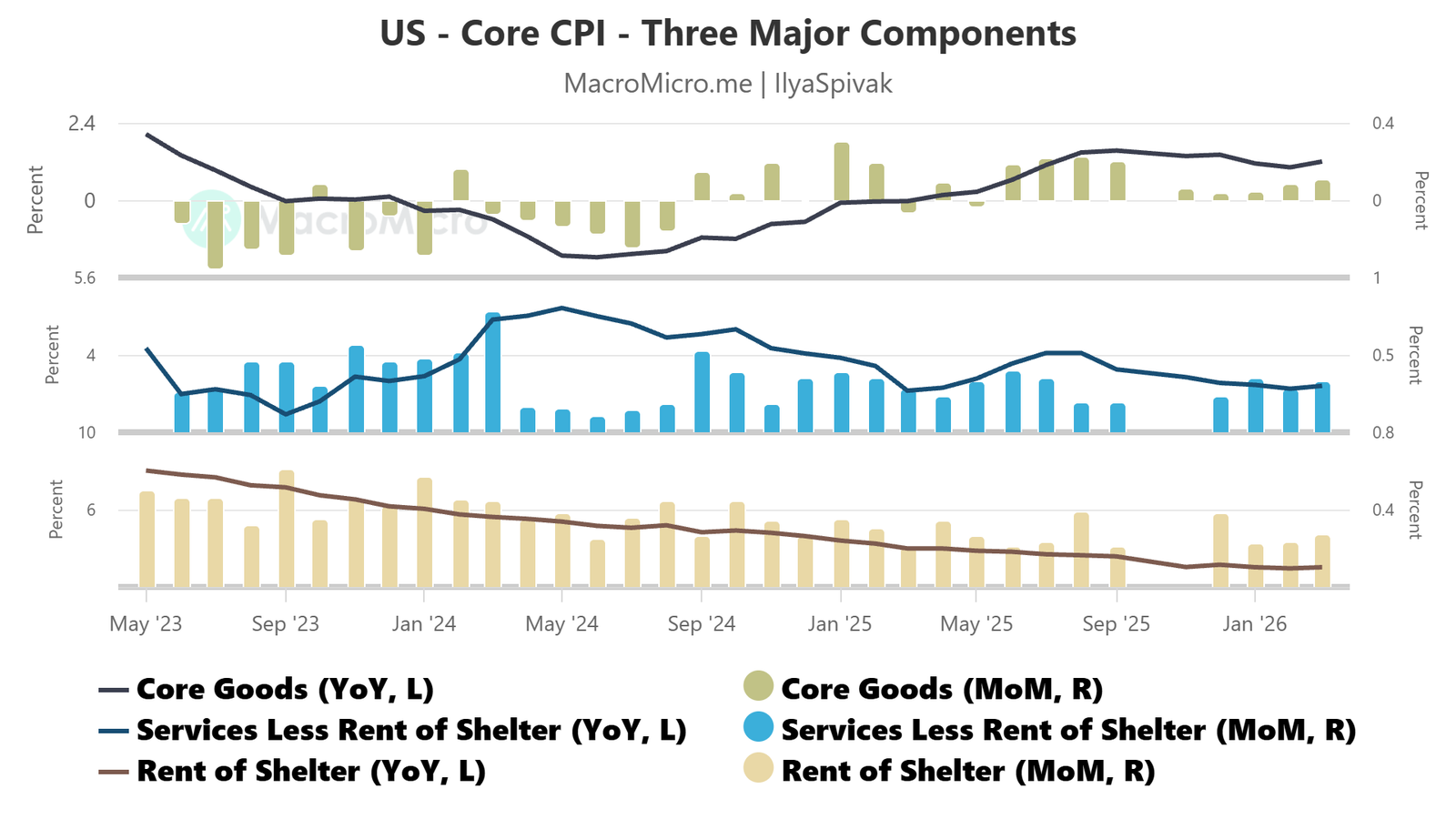

The Fed’s inflation problem is broader than the oil shock

The Fed’s March policy statement, issued just two weeks into the Iran war, was deliberately spare, noting only that the conflict’s implications for the US economy are uncertain. Governor Christopher Waller, who had been voting for cuts, moved to neutral. Stephen Miran remained the lone dove, but even his conviction has moderated recently.

Speaking at the press conference following that meeting of the Federal Open Market Committee (FOMC), Chair Jerome Powell did not pull punches was on inflation. He flagged an unwelcome rise in price growth expectations, which he linked to goods inflation linked to tariffs.

The Fed has argued for over a year that this would prove transitory, but the latest data suggests otherwise. Stripping out energy and food, goods inflation began rising again at the start of the year. Services inflation posted some of its strongest monthly gains since mid-2025 in the first quarter, and housing inflation has steadily perked up.

On top of that comes the energy shock. With a typical one-month lag from crude prices to the US consumer price index (CPI), the run-up in oil prices is just starting to appear. The war-linked spike should make its debut in April’s readings. US PMI data is echoing the trend, with implying price pressure at its most potent since 2022.

The real question is whether Powell will bail out markets

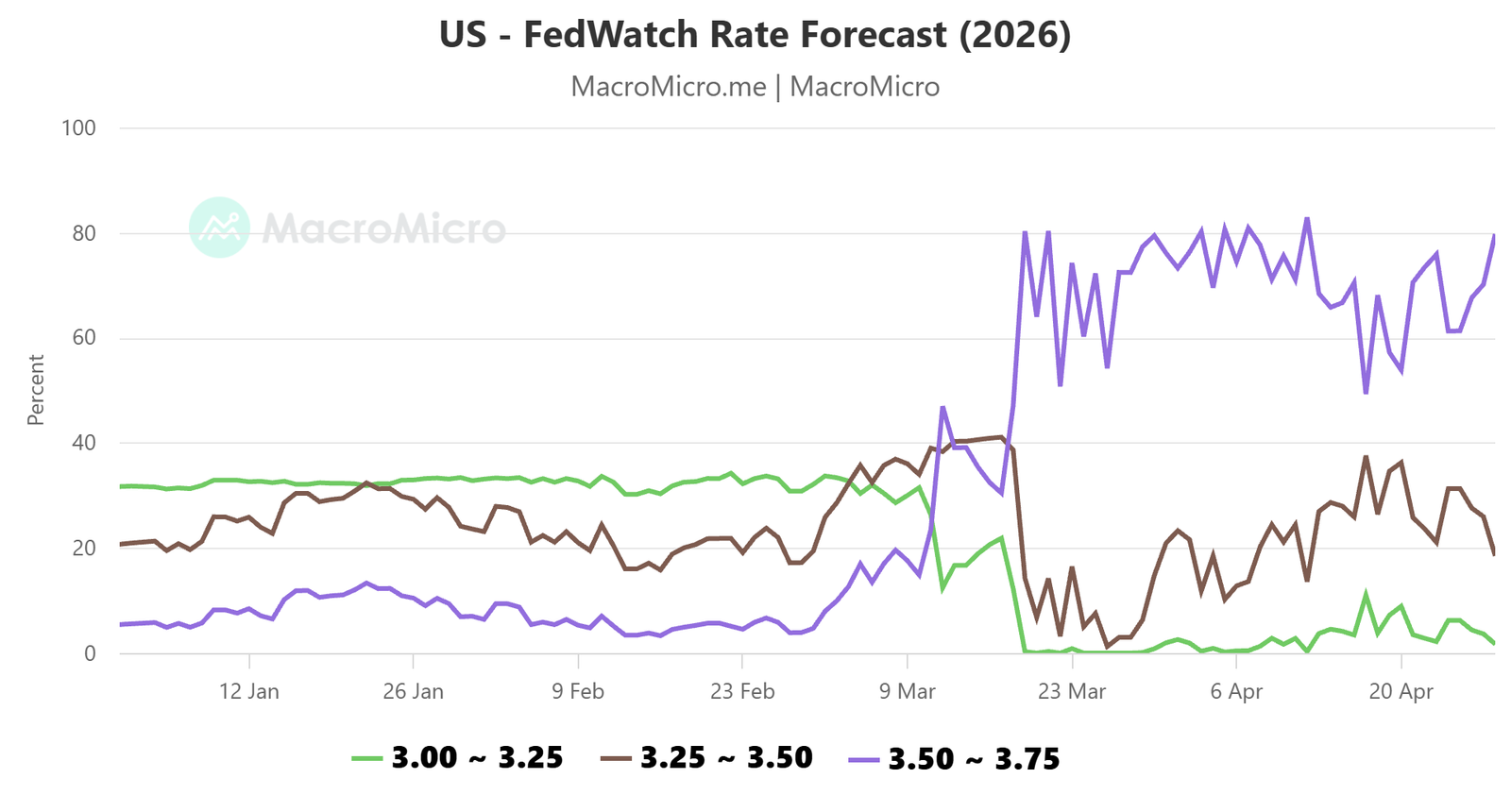

Fed funds futures reflect a commanding 80% probability that rates will not move at all in 2026. Even one cut by year-end is a dwindling prospect, and two cuts have effectively dropped out of speculation. The soonest that a cut may appear is October.

In other words, traders already know that the central bank is not primed for a move now or in the near future. This means that the policy decision itself is probably an afterthought.

What markets really want from the Fed is insurance. Much of the rebound from last April’s tariff-driven panic, when stocks, bonds, and the dollar fell together in a brief “sell America” moment, was built on the assumption that the Fed stands ready to step in if conditions deteriorate. If officials signal a high bar for such action, stocks may find themselves looking unsupported just as the inflation pipeline gets noisier and tech earnings land.

Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOG), and META all report after the close on Wednesday, with Apple (AAPL) following on Thursday. The latest melt-up seems to have a strong batch of numbers already be priced in, and any disappointment could accelerate what the momentum indicators are hinting at.

The question is not whether the Fed will cut. It is whether stocks are about to lose the safety net they have been quietly counting on.

Ilya Spivak, tastylive Head of Global Macro, has over 15 years of experience in trading strategy. He specializes in identifying thematic moves in currencies, commodities, interest rates and equities. He hosts Macro Money and co-hosts Overtime, Monday-Thursday. @Ilyaspivak

For live daily programming, market news and commentary, visit tastylive.com or @tastyliveshow on YouTube

Trade with a better broker, open a tastytrade account today. tastylive, Inc. and tastytrade, Inc. are separate but affiliated companies.

Options involve risk and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before deciding to invest in options.

© copyright 2013 – 2026 tastylive, Inc.