These are the early headlines and other items poised to influence the market at the start of trading Wednesday. As we share this collection of market drivers, U.S. equity futures point to a modest decline at the open.

1. US President Donald Trump played down the prospect of renewed fighting in the war with Iran, even as questions remain over Tehran’s nuclear program and access to the Strait of Hormuz. Speaking to ABC News on Tuesday, Trump said extending a ceasefire that expires next week may not be necessary, hinting at near-term progress toward a deal to end the near seven-week conflict. In a Fox Business interview, he said the war is “close to over.” (Bloomberg)

The stock market has been on a tear over the last several days, with the Nasdaq’s 10-day winning streak its best run since 2021 and the S&P 500 closing in on a new all-time high. While great for investors and the Pro Portfolio, as it pulled ahead of the S&P 500 on a YTD basis, the market has also gone from being oversold to, based on some indicators, once again overbought. In the past when the market has whipsawed like this, it hasn’t taken much to foster at least a modest pullback.

This time around, we have Q1 2026 earnings season and how it will showcase the impact of higher energy prices, supply disruptions, and tariffs compared to consensus EPS expectations that moved higher in recent weeks. Recent earnings reports that have bested market expectations have not all been met with positive stock price movements, and we view that as a sign to remain cautious in the near term. To that we can add any potential hiccup in U.S.-Iran conversations that alter the market’s expectation for a near-term resolution.

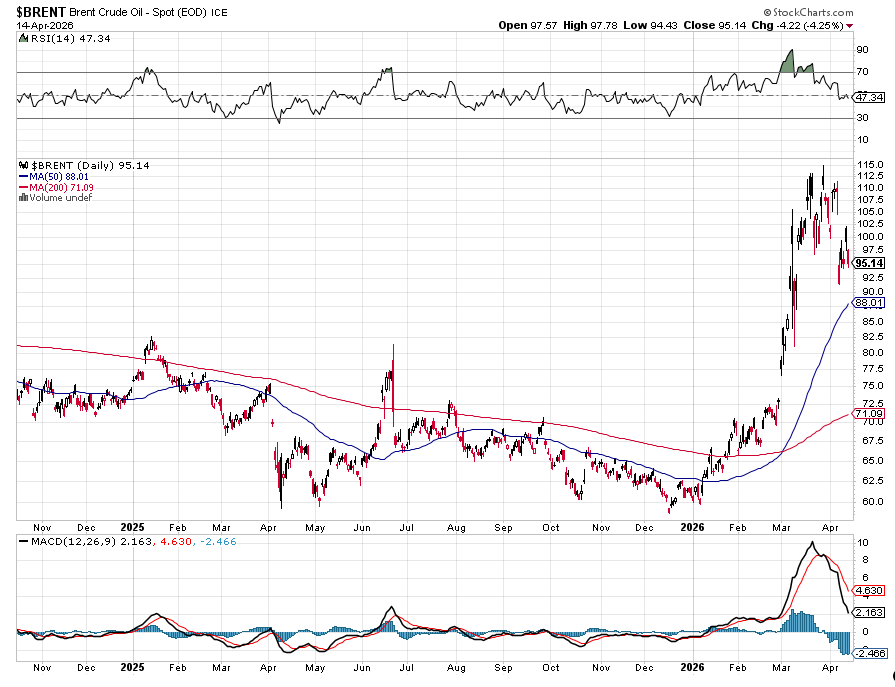

2. The International Monetary Fund cut its growth outlook on Tuesday due to Middle East war-driven energy price spikes but said the world was already drifting toward a more adverse scenario with much-weaker growth as Strait of Hormuz shipping disruptions continue… The IMF chose the most benign scenario for its World Economic Outlook “reference forecast,” which assumes a short-lived conflict and oil prices normalizing in the second half of 2026, with an $82 per-barrel average for the year – well below Tuesday’s benchmark Brent crude futures price of around $96.00. (Reuters)

Our view has been that where oil, related energy and petrochemical prices settle out once the U.S.-Iran War is over, will be part of our focus. If the IMF’s $82 forecast is correct, that would mean Brent crude prices settle out well above early 2026 levels and Q2 to Q1 2025.

3. Meta will work with chip designer Broadcom to produce several generations of custom artificial intelligence processors under an expanded deal as the social media giant races to build out the computing capacity needed to power AI features across its apps. Tuesday’s announcement extends the tie-up until 2029 and includes an initial commitment of over one gigawatt of computing capacity, enough to power roughly 750,000 U.S. homes on average. (Reuters)

Another positive data point for the custom AI chip market following bullish comments from Amazon (AMZN) that popped shares of Portfolio holding Marvell (MRVL) . We see this as Meta (META) continuing to lock in needed capacity as it builds out its AI efforts in the coming years. It also backs the robust multi-year outlook issued by Broadcom (AVGO) when it reported quarterly results just a few weeks ago.

4. ASML Holding NV raised its full-year sales forecast as the surge in global artificial intelligence spending fuels semiconductor production and boosts demand for the company’s advanced chipmaking machines. Net sales will be between €36 billion ($42.4 billion) to €40 billion this year, the Dutch company said in a statement Wednesday. That compares to a previous range of €34 billion to €39 billion… “We expect in fact that the supply will not meet the demand for the foreseeable future… “This is creating a strong constraint in the end markets from AI to mobile and PC.” (Bloomberg)

This speaks to the tight chip industry capacity that led the Portfolio to add shares of Applied Materials (AMAT) as well as the mix shift in capacity to AI and data center from PC, smartphone, and other connected devices. It also reaffirms our decision to close out our Qualcomm (QCOM) position back in January for an ample gain well before their collapse over the last few months.

5. Uber has committed more than $10bn to buying thousands of autonomous vehicles and taking stakes in their developers, breaking from its asset-light “gig economy” business model to avoid disruption from robotaxis. The ride-hailing app has aggressively increased its dealmaking over the past year, announcing partnerships with more than a dozen providers, including China’s Baidu and US-based Rivian, as well as plans to launch robotaxi services in at least 15 cities in 2026. These deals put Uber on track to invest more than $2.5bn in equity stakes and spend over $7.5bn on robotaxi fleets in the next few years… (FT)

This helps answer a question that we’ve debated as to whether Uber (UBER) would shift from its current asset-lite strategy to one that is more capital-intensive. The company’s commitment also serves as a confirmation point for autonomous vehicles, one that we’re covered with through our positions in Alphabet (GOOGL) , Amazon, and Nvidia (NVDA) .

6. President Donald Trump’s tariffs may be restored by July to the levels in place before the Supreme Court struck down many of his levies, Treasury Secretary Scott Bessent said…. After the Supreme Court struck down many of his global tariffs, Trump imposed a temporary 10% tariff that covers many imports. That levy is set to expire on July 24. (Bloomberg)

While the market is eyeing oil prices moving off peak level, but perhaps not as low as we’ve seen earlier this year, the resumption of tariffs has the potential to keep inflation pressures blowing. The question is whether Trump will utilize this stick to foster trade deals that have yet to be finalized. Based on what we’ve seen over the last year, the odds are more likely than not.

7. Economic data today per TipRanks: MBA Mortgage Application Index (Weekly), Empire State Manufacturing Index (April), Import/Export Prices (March), NAHB Housing Market Index (April), EIA Crude Oil Inventories (Weekly), Beige Book (April).

8. Companies reporting today per TipRanks: AM – ASML (ASML) , Bank of America (BAC) , Morgan Stanley (MS) , PNC Financial (PNC) , Progressive (PGR) . PM – J.B. Hunt (JBHT) .

Related: Amazon’s $11 Billion Satellite Expansion Brings Key Agreement With Apple

At the time of publication, TheStreet Pro Portfolio was long AMZN, AVGO, BAC, GOOGL, META, MRVL, MS, and NVDA.