For most retired Americans, their monthly Social Security check is an indispensable source of income. Based on annually conducted surveys over the course of more than two decades, no fewer than 80% of then-current retirees rely on their monthly benefit to help cover their expenses.

Given how important America’s top retirement program is to the financial health of our nation’s retired workers, workers with disabilities, and survivor beneficiaries, you’d think that ensuring the sustainability of the current payout schedule would be paramount. However, Social Security’s foundation has been showing signs of cracking for decades.

America’s top retirement program has more than $22 trillion in long-term unfunded obligations

For more than eight decades, the Social Security Board of Trustees has released an annual report that takes an under-the-hood look at the program’s finances, as well as examines its short-term (10-year) and long-term (75-year) outlook. These outlooks factor in ongoing demographic changes, as well as shifts in fiscal and monetary policy, to determine how sustainable the existing payout schedule is for current and future beneficiaries.

Every year since 1985, the Trustees Report has cautioned that Social Security would be facing some degree of long-term unfunded obligation. In simpler terms, forecast revenue collection in the 75 years following the release of a Trustees Report was not expected to cover projected outlays. As of 2023, the trustees estimate Social Security is contending with a $22.4 trillion funding shortfall through 2097.

To provide clarity, this doesn’t mean Social Security is facing bankruptcy or insolvency. Rather, it means the current payout schedule, including annual cost-of-living adjustments (COLAs), can’t be sustained, based on current projections. If the asset reserves of the Old-Age and Survivors Insurance (OASI) Trust Fund are exhausted by 2033, as the 2023 Trustees Report portends, retired workers and survivor beneficiaries could see their benefits reduced by up to 23%.

The blame for this predicament has nothing to do with Congress stealing Social Security’s asset reserves, undocumented workers, or any other myths that may prevail on social media message boards. Rather, the bulk of Social Security’s troubles can be traced to demographic changes.

The best example is the steady retirement of baby boomers from the labor force. While a boom in births following World War II pumped up Social Security’s asset reserves during the 1990s and early 2000s, the retirement of these workers is now weighing heavily on the worker-to-beneficiary ratio.

A lesser-known reason for Social Security’s financial woes, which I recently covered, is the 25-year decline in legal migration into the United States. America’s top retirement program counts on a certain number of younger people migrating into the U.S. each year. Younger people will remain in the workforce for decades, thereby providing much-needed payroll tax revenue for Social Security.

But the under-the-radar problem that can no longer be swept under the rug is income inequality.

Income inequality is no longer a problem that can be ignored

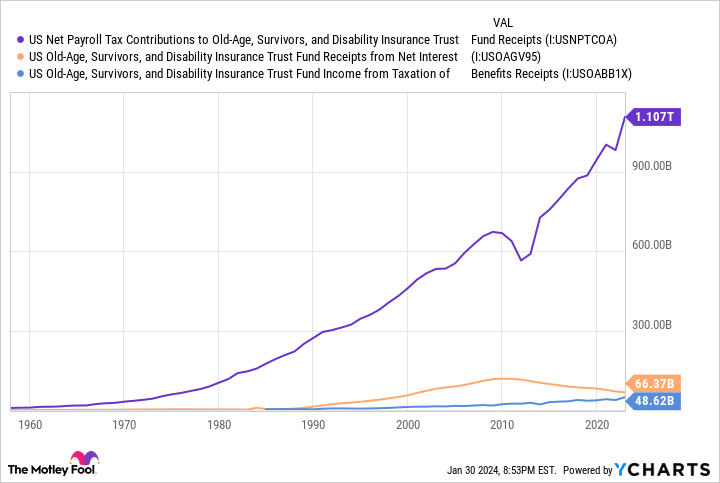

In 2022, Social Security brought in approximately $1.222 trillion in revenue from three funding sources (payroll tax contribution, net interest on asset reserves, and the taxation of benefits). The payroll tax accounted for about 90% ($1,107 trillion) of this revenue.

Social Security’s 12.4% payroll tax is applicable to earned income — wages and salary, but not investment income — between $0.01 and $168,600, as of 2024. Whereas the self-employed are responsible for the entirety of this 12.4% tax, employees split this tax down the middle with their employer, with each covering 6.2%.

Close to 94% of working Americans earn less than the maximum taxable earnings cap (the $168,600 figure noted above) in a given year. This means they’re paying into Social Security with every dollar they earn.

On the other hand, 6.2% of working Americans in 2021 achieved what was then the maximum taxable earnings cap. For these individuals, payroll taxation is exempted above this threshold. It should also be noted that this threshold tends to rise in lockstep with the National Average Wage Index (NAWI) most years.

In 1985, 88.9% of all earned income was exposed to the payroll tax and approximately 6.5% of workers achieved maximum taxable earnings. But as of 2021, just 81.4% of taxable earnings was applicable to the payroll tax, with 6.2% reaching the maximum taxable earnings cap.

Given that $8.4 trillion in total income on Form 1040s were wages and salaries in tax year 2020 — I know this isn’t an apples-to-apples comparison, but it often takes the IRS a few years to compile and publish encompassing tax statistics — it means roughly $1.56 trillion in earned income is escaping the payroll tax each year. That’s almost $194 billion in estimated payroll tax revenue lost to growing income inequality in 2021 alone.

If wage and salary growth for high earners continues to vastly outpace the near-annual increases in the maximum taxable earnings cap, Social Security’s income inequality problem will only worsen.

Taxing the rich may sound great on paper, but it’s not a cut-and-dried solution

One of the lawmakers who’s recognized this Social Security dilemma and wants to tackle it head on is President Joe Biden.

Prior to being elected president in November 2020, Biden proposed a four-point plan to strengthen the program. The flagship change offered by then-candidate Biden was to reinstate the payroll tax on earned income above $400,000, while creating a doughnut hole between the maximum taxable earnings cap and $400,000 where earned income would remain exempt. Since the NAWI rises most years, this doughnut hole would be expected to close over the course of a few decades, thereby exposing all wages and salary to the payroll tax.

While taxing the rich may sound great on paper, it’s a solution that’s not as cut-and-dried as it appears.

To begin with, taxing high earners doesn’t completely resolve Social Security’s funding obligation shortfall. Simply taxing all earned income and making no other changes to the program would extend the life of Social Security’s asset reserves by about 35 years. Meanwhile, if the other tenets of Biden’s proposal were implemented, the ultimate benefit is an extension of Social Security’s asset reserves by about five years. Although taxing the rich does extend the life of the program’s asset reserves, it’s not a cure-all by itself.

Another problem with increasing taxation on high earners is that they’re liable to adjust how they generate income to lessen their tax burden. This could mean fewer hours worked or possibly an earlier retirement. Either way, it results in less production for the U.S. economy, which would be a net negative for long-term gross domestic product.

An argument can also be made that the rich are already paying their fair share into Social Security. Just as there’s a ceiling on the amount of earnings that can be taxed, there’s also a cap on monthly benefits at full retirement age ($3,822 a month in 2024). Increasing taxation on high earners without providing a penny in additional benefits doesn’t make much sense.

While I believe there’s a good likelihood that an eventual solution to Social Security’s long-term funding shortfall will involve some level of increased payroll taxation, either on high earners or all workers, it would be naïve to overlook the reality that other changes will need to be made to cover a $22.4 trillion, and growing, long-term cash shortfall.

The $21,756 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $21,756 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Simply click here to discover how to learn more about these strategies.

The Motley Fool has a disclosure policy.

Social Security Has an Income Inequality Problem, and It Can’t Be Swept Under the Rug Any Longer was originally published by The Motley Fool