Over the past four years, volatility has ruled the roost on Wall Street. The 127-year-old Dow Jones Industrial Average (DJINDICES: ^DJI), benchmark S&P 500 (SNPINDEX: ^GSPC), and growth-powered Nasdaq Composite (NASDAQINDEX: ^IXIC) have traded off bear and bull markets in successive years since this decade began.

Even though Wall Street has proved to be a bona fide long-term wealth creator, it doesn’t stop investors from trying to gain an edge by knowing which direction the Dow Jones, S&P 500, and Nasdaq Composite will head next.

Truth be told, there is no such thing as a predictive indicator or economic data point that can, with 100% accuracy, forecast which direction stocks will move next. There are, however, select metrics and forecasting tools that have phenomenal track records and do strongly correlate with previous directional moves in the U.S. economy and/or stock market. It’s these indicators and metrics that are of particular interest to investors.

Perhaps the most-telling economic data point at the moment is the U.S. money supply.

U.S. money supply hasn’t done this in more than 90 years

Although there are number of prominent measures of money supply, most economists and investors tend to focus on M1 and M2. The former is a measure of cash and coins in circulation, as well as demand deposits in a checking account. It’s money that can be easily accessed and spent by consumers.

Meanwhile, M2 money supply accounts for everything in M1 and adds in savings accounts, money market funds, and certificates of deposit (CDs) below $100,000. While this money can also be spent by consumers, it requires a little extra work to access it. It’s M2 that’s currently in focus.

Most economists and investors rarely pay much attention to M2 given that money supply rises so consistently over long periods. Growing economies require more capital in circulation to facilitate transactions, which results in M2 increasing virtually every year.

But it’s those rare instances where M2 does decline, and consumers are forced to forgo some of their purchases, that have resulted in trouble for the U.S. economy and Wall Street.

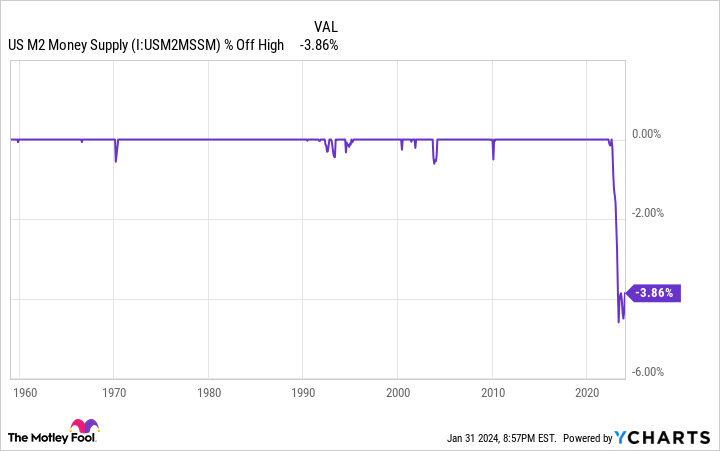

Based on monthly data from the Board of Governors of the Federal Reserve System, U.S. M2 money supply peaked at roughly $21.7 trillion in July 2022. As of December 2023, M2 sat at approximately $20.87 trillion.

M2 has fallen by 1.68% on a year-over-year basis and 3.86% since its summer 2022 peak. This represents the first meaningful decline in M2 since the Great Depression.

On a nominal basis, a 3.86% drop probably doesn’t sound like much. In fact, with M2 expanding by a record 26% on a year-over-year basis during the pandemic, a reasonable argument could be made that a 3.86% retracement since mid-2022 is nothing more than a reversion to the mean for money supply. But when examined historically, M2 drops of at least 2% have been telltale signs of an economic downturn.

Putting aside minor year-over-year declines, there have been only five instances, when back-tested to 1870 — based on data from Reventure Consulting CEO Nick Gerli — where M2 has fallen by at least 2%: 1878, 1893, 1921, 1931-1933, and July 2022-currently. All four previous instances led to deflationary depressions and a sizable increase in the U.S. unemployment rate.

WARNING: the Money Supply is officially contracting. 📉

This has only happened 4 previous times in last 150 years.

Each time a Depression with double-digit unemployment rates followed. 😬 pic.twitter.com/j3FE532oac

— Nick Gerli (@nickgerli1) March 8, 2023

Understandably, the Federal Reserve’s knowledge of monetary policy, and the federal government’s use of fiscal policy, have evolved considerably from a century ago. In fact, the depressions in 1878 and 1893 occurred prior to the creation of the nation’s central bank. With the tools available now, it’s highly unlikely that a depression would take place.

Nevertheless, history suggests that declines in M2 money supply shouldn’t be ignored. If M2 shrinks and the prevailing inflation rate remains above historic norms, it’s a recipe for consumers to purchase fewer goods and services. In other words, it’s a formula for a recession.

Since September 1929, in the neighborhood of two-thirds of the S&P 500’s drawdowns have occurred after, not prior to, an official recession being declared by the National Bureau of Economic Research. Put simply, if a recession takes shape, stocks would be expected to perform poorly.

Money-based metrics are a clear concern for the U.S. economy and stocks

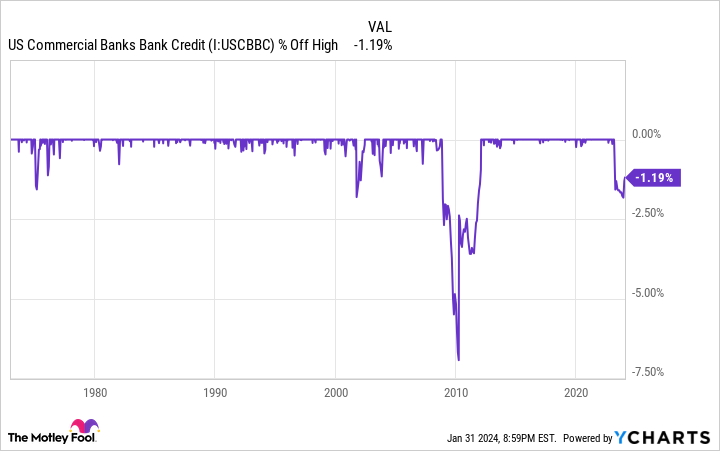

What’s particularly worrisome for the U.S. economy in 2024 is that M2 isn’t the only money-based metric offering an ominous warning. Commercial bank credit is another data point worth eyeing that’s recently made history.

Commercial bank credit includes all loans, leases, and securities (e.g., mortgage-backed securities) held by U.S. commercial banks. Similar to M2, commercial bank credit has grown almost without fail since it was first reported in January 1973.

A steady increase in commercial bank credit makes sense for two reasons. First, bank loan and lease portfolios are going to grow in lockstep with the U.S. economy, which spends a disproportionate amount of time expanding, relative to contracting. And second, banks are incentivized to lend to offset the liability costs associated with taking in deposits (e.g., interest expenses).

But when commercial bank credit meaningfully drops, caveat emptor!

Spanning more than a half-century, there have been only three instances when commercial bank credit retraced more than 2% from its all-time high:

-

A maximum decline of 2.09% during the dot-com bubble (October 2001).

-

A peak 6.94% nosedive shortly after the Great Recession (March 2010).

-

A drop of 2.07%, as of November 2023.

As you’ll note, commercial bank credit has now retraced almost half of its decline, which began in mid-February 2023, just prior to the short-lived regional banking crisis.

Nevertheless, what these drops have signaled for more than 50 years is that banks are purposefully tightening their lending standards. If businesses have reduced access to capital, it means less in the way of hiring, acquisitions, and innovation. That’s bad news for both the U.S. economy and the stock market.

Not surprisingly, the two previous instances of a greater than 2% drop in commercial bank credit have correlated with a practical halving of the S&P 500.

History repeating itself is a blessing in disguise for long-term investors

Both money-based metrics and a couple of predictive indicators appear to signal that a recession, and possibly even a bear market, is in the cards for the U.S. economy and Wall Street’s major stock indexes in 2024. But even if history repeats itself, it’ll be nothing more than a blessing in disguise for long-term investors.

To be clear, I’m not saying recessions are fun. They’re events that lead to higher unemployment and reduce or remove wage growth from the equation. But inevitable economic downturns are also short-lived.

Since World War II ended in September 1945, the U.S. has worked its way through 12 official recessions. Just three of these 12 recessions lasted at least 12 months, and none of them surpassed 18 months.

On the other side of the coin, most periods of expansion have lasted multiple years. Betting on the American economy to succeed, which is a core Warren Buffett philosophy, has always been a smart move for patient investors.

This philosophy works with stocks, too. Even though we’re never going to know ahead of time precisely when the Dow Jones, S&P 500, or Nasdaq Composite will enter a correction or bear market (or how long that decline will last), we do know that every downturn is eventually cleared away by a bull market rally. This is what makes buying stocks during pullbacks such a blessing in disguise for patient investors.

But you don’t have to take my word for it. This past June, researchers at Bespoke Investment Group took the time to calculate how long bear and bull markets stick around for the broad-based S&P 500.

As you can see from Bespoke’s post, the average S&P 500 bear market dating back to the start of the Great Depression in September 1929 has lasted about 9.5 months (286 calendar days). Comparatively, the average bull market has endured for roughly 3.5 times as long (1,011 calendar days). Even though Wall Street doesn’t adhere to averages, close to a century of historic performance decisively shows that bull markets last considerably longer than bear markets.

As of this moment, nothing is etched in stone for 2024. But if the decline in M2, once again, correlates to a downturn in the U.S. economy, long-term investors are well positioned for success.

10 stocks we like better than Walmart

When our analyst team has an investing tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Walmart wasn’t one of them! That’s right — they think these 10 stocks are even better buys.

*Stock Advisor returns as of 1/29/2024

Sean Williams has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

U.S. Money Supply Is Doing Something No One Has Seen Since the Great Depression, and It Implies a Big Move to Come in Stocks was originally published by The Motley Fool